Understanding Credit Card Debt Consolidation

Understand the key differences between debt settlement and bankruptcy to make an informed decision for your debt relief.

Understand the key differences between debt settlement and bankruptcy to make an informed decision for your debt relief. Facing overwhelming debt can feel like navigating a dense fog, with every path seeming equally daunting. When you're drowning in bills and collection calls, two common lifelines often emerge: debt settlement and bankruptcy. Both offer a way out, but they are vastly different in their approach, impact, and long-term consequences. Choosing between them is a monumental decision that can shape your financial future for years to come. This comprehensive guide will cut through the confusion, comparing debt settlement and bankruptcy in detail, exploring their pros and cons, and helping you determine which option might be the better fit for your unique situation.

Debt Settlement vs Bankruptcy Which is Better

Understanding Debt Settlement What It Is and How It Works

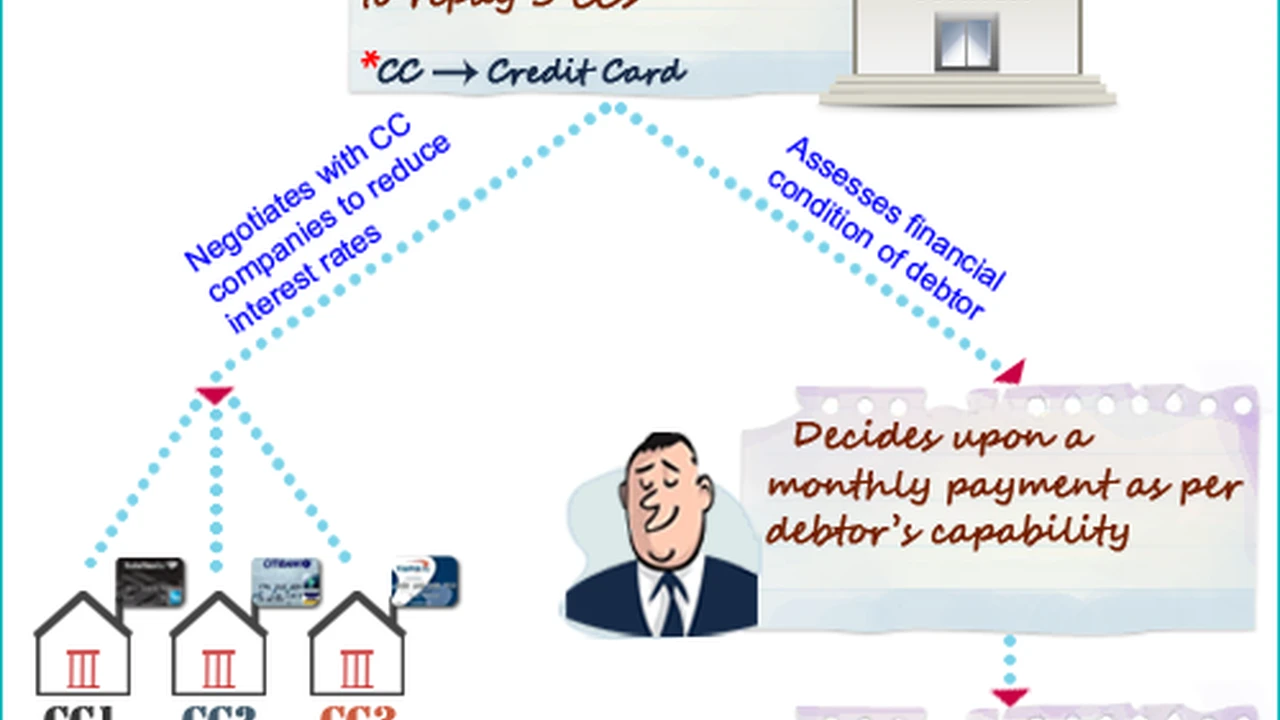

Debt settlement, sometimes referred to as debt negotiation, is a process where you or a debt settlement company negotiates with your creditors to pay back a portion of your outstanding debt, rather than the full amount. The goal is to reach an agreement where the creditor accepts a lump sum payment that is less than what you originally owed, thereby resolving the debt. This typically involves stopping payments to your creditors and instead depositing money into a special savings account managed by the debt settlement company. Once enough funds have accumulated, the company attempts to negotiate with your creditors. Creditors, facing the possibility of receiving nothing if you declare bankruptcy, may be willing to settle for a reduced amount.The Debt Settlement Process Step by Step

The debt settlement process usually unfolds in several stages:

- Initial Consultation and Assessment: You'll typically start with a free consultation with a debt settlement company. They will review your financial situation, including your income, expenses, and the types and amounts of your debts, to determine if debt settlement is a viable option for you.

- Enrollment and Account Setup: If you decide to proceed, you'll enroll in their program. This often involves opening a special savings account (an escrow-like account) where you'll make regular, agreed-upon payments to the debt settlement company.

- Stopping Payments to Creditors: A crucial and often controversial step is that you will be advised to stop making payments directly to your creditors. The money you would have paid to creditors is instead directed into your dedicated savings account. This is done to build up a lump sum for settlement and to signal to creditors that you are in financial distress, making them more amenable to negotiation.

- Negotiation Phase: While you're building up funds, the debt settlement company will begin negotiating with your creditors. This can be a lengthy process, often taking months or even years. Creditors are typically more willing to negotiate once an account is significantly delinquent.

- Settlement Agreement: Once a settlement is reached, the debt settlement company will use the funds from your savings account to pay the agreed-upon reduced amount to the creditor. You will receive documentation confirming the debt has been settled.

- Fees: Debt settlement companies charge fees, usually a percentage of the enrolled debt or a percentage of the amount saved. These fees are typically collected as settlements are reached.

Pros and Cons of Debt Settlement for Your Financial Future

Like any financial strategy, debt settlement comes with its own set of advantages and disadvantages:

Advantages of Debt Settlement

- Potential for Significant Debt Reduction: You could end up paying back significantly less than what you originally owed, sometimes as little as 40-60% of the original debt.

- Avoid Bankruptcy: For many, avoiding bankruptcy is a primary goal, and debt settlement offers an alternative path to debt relief.

- One Monthly Payment: You make one consolidated payment to the debt settlement company, which can simplify your finances.

- Faster Resolution Than Minimum Payments: While not instant, debt settlement can resolve your debts faster than making minimum payments, which often barely cover interest.

Disadvantages of Debt Settlement

- Significant Negative Impact on Credit Score: Stopping payments to creditors will severely damage your credit score. Accounts will be reported as delinquent, charged off, or settled for less than the full amount, all of which are negative marks. This impact can last for up to seven years.

- Collection Calls and Lawsuits: While you're not paying creditors, you will likely face aggressive collection calls. Creditors may also sue you for the unpaid debt, which can lead to wage garnishment or liens if they win a judgment. Debt settlement companies typically do not protect you from lawsuits.

- Tax Implications: The amount of debt forgiven through settlement is often considered taxable income by the IRS. You may receive a 1099-C form from creditors, and you'll need to report this income on your tax return, potentially increasing your tax liability.

- High Fees: Debt settlement companies charge fees, which can be substantial and eat into your savings.

- No Guarantee of Success: Creditors are not obligated to settle, and some may refuse to negotiate. There's a risk that not all your debts will be settled, leaving you with unresolved obligations.

- Long Process: Debt settlement can take several years to complete, during which your credit remains severely damaged.

Exploring Bankruptcy Chapter 7 and Chapter 13 Explained

Bankruptcy is a legal process designed to help individuals and businesses who cannot repay their outstanding debts. It provides a fresh financial start by either discharging certain debts (Chapter 7) or reorganizing them into a manageable payment plan (Chapter 13). Bankruptcy is a federal court proceeding, and its rules are governed by the U.S. Bankruptcy Code.Chapter 7 Bankruptcy Liquidation and Discharge

Chapter 7 bankruptcy, often referred to as 'liquidation bankruptcy,' is designed for individuals with limited income who cannot afford to repay their debts. The primary goal of Chapter 7 is to discharge (eliminate) most unsecured debts, such as credit card debt, medical bills, and personal loans. In exchange, a bankruptcy trustee may sell some of your non-exempt assets to pay off creditors. However, most Chapter 7 filers are able to keep all of their property due to state and federal exemption laws.

Key Aspects of Chapter 7

- Means Test: To qualify for Chapter 7, you must pass a 'means test,' which compares your income to the median income in your state. If your income is too high, you may be required to file Chapter 13.

- Asset Liquidation (Rare): A trustee is appointed to oversee your case. They will review your assets and determine if any non-exempt property can be sold to pay creditors. In the vast majority of consumer Chapter 7 cases, all assets are exempt, meaning the debtor keeps everything.

- Debt Discharge: Most unsecured debts are discharged, meaning you are no longer legally obligated to pay them. Certain debts, like most student loans, recent taxes, child support, and alimony, are typically not dischargeable.

- Automatic Stay: Once you file, an 'automatic stay' goes into effect, immediately stopping most collection activities, including lawsuits, wage garnishments, and collection calls.

- Credit Counseling: You must complete a credit counseling course before filing and a debtor education course before your debts can be discharged.

- Duration: The entire Chapter 7 process typically takes about 3-6 months.

Chapter 13 Bankruptcy Reorganization and Repayment Plan

Chapter 13 bankruptcy, known as 'reorganization bankruptcy,' is for individuals with regular income who can afford to repay some or all of their debts over time. Instead of liquidating assets, Chapter 13 involves creating a repayment plan, typically lasting three to five years, during which you make regular payments to a bankruptcy trustee. The trustee then distributes these payments to your creditors.

Key Aspects of Chapter 13

- Repayment Plan: You propose a repayment plan to the court, outlining how you will pay back your debts over a set period. The plan must be approved by the court.

- Retain Assets: Unlike Chapter 7, you get to keep all of your property, including non-exempt assets, as long as you make your plan payments.

- Curing Defaults: Chapter 13 can be used to catch up on past-due mortgage payments, car loans, and other secured debts, preventing foreclosure or repossession.

- Debt Limits: There are limits on the amount of secured and unsecured debt you can have to qualify for Chapter 13.

- Automatic Stay: Similar to Chapter 7, an automatic stay goes into effect upon filing, stopping collection activities.

- Credit Counseling and Debtor Education: These courses are also required for Chapter 13 filers.

- Duration: The repayment plan lasts for three to five years, after which any remaining dischargeable debts are eliminated.

Pros and Cons of Bankruptcy for Debt Relief

Bankruptcy, while a powerful tool, carries significant implications:

Advantages of Bankruptcy

- Immediate Relief from Creditors: The automatic stay provides immediate protection from collection calls, lawsuits, wage garnishments, and foreclosures.

- Debt Discharge: Chapter 7 can eliminate most unsecured debts entirely, offering a true fresh start. Chapter 13 can significantly reduce and reorganize debts.

- Structured Repayment (Chapter 13): Chapter 13 provides a court-supervised plan to repay debts, often at a reduced amount and without interest on unsecured debts.

- Protection of Assets (Chapter 13): You can keep all your property in Chapter 13. In Chapter 7, most filers keep all their property due to exemptions.

- Legal Protection: Bankruptcy is a legal process that offers defined protections and a clear path to debt resolution.

Disadvantages of Bankruptcy

- Severe Credit Score Damage: Bankruptcy remains on your credit report for 7-10 years (10 years for Chapter 7, 7 years for Chapter 13), making it difficult to obtain new credit, loans, or even housing.

- Public Record: Bankruptcy filings are public record.

- Loss of Assets (Chapter 7, if non-exempt): While rare for most consumers, there is a possibility of losing non-exempt assets in Chapter 7.

- Not All Debts Discharged: Certain debts, like student loans, child support, alimony, and some taxes, are generally not dischargeable in bankruptcy.

- Cost: There are court filing fees and attorney fees associated with bankruptcy, which can be substantial.

- Emotional Toll: Filing for bankruptcy can be a stressful and emotionally challenging experience.

- Future Credit Challenges: Even after discharge, rebuilding credit can be a long and arduous process.

Comparing Debt Settlement and Bankruptcy Key Differences and Considerations

To make an informed decision, it's crucial to understand the fundamental differences between these two debt relief options:

Impact on Credit Score and Credit Report

Both debt settlement and bankruptcy will severely damage your credit score, but the nature and duration of the impact differ. Debt settlement involves accounts being reported as delinquent, charged off, or settled for less than the full amount, which stays on your report for seven years. Bankruptcy, particularly Chapter 7, is often considered the most severe negative mark and remains on your report for 10 years (Chapter 13 for 7 years). While both are detrimental, bankruptcy offers a clean slate sooner for many debts, whereas settled accounts can still appear as negative marks for the full seven years.

Cost and Fees Associated with Each Option

Debt settlement companies typically charge fees based on a percentage of the enrolled debt or the amount saved. These fees can range from 15% to 25% of the total debt. For example, if you have $50,000 in debt and the company charges 20%, you could pay $10,000 in fees. Bankruptcy involves court filing fees (around $338 for Chapter 7, $313 for Chapter 13) and attorney fees, which can range from $1,500 to $4,000 or more, depending on the complexity of the case and your location. While bankruptcy fees can seem high upfront, they are often a fixed cost, whereas debt settlement fees can accumulate over time.

Protection from Creditors and Collection Activities

This is a major differentiator. When you file for bankruptcy, an 'automatic stay' immediately goes into effect, legally stopping most collection activities, including phone calls, letters, lawsuits, and wage garnishments. This provides immediate and comprehensive protection. In debt settlement, there is no such legal protection. While the debt settlement company may advise you to stop paying, creditors are still legally entitled to pursue collection efforts, including lawsuits, until a settlement is reached and paid. This means you could still face aggressive collection calls and even legal action during the debt settlement process.

Tax Implications of Debt Forgiveness

A critical consideration for debt settlement is the tax implication. When a creditor forgives a portion of your debt (i.e., settles for less than the full amount), the IRS generally considers the forgiven amount as taxable income. You will typically receive a Form 1099-C, 'Cancellation of Debt,' from the creditor, and you'll need to report this on your tax return. This can lead to an unexpected tax bill. There are exceptions, such as if you were insolvent at the time the debt was forgiven, but it's crucial to consult with a tax professional. In bankruptcy, discharged debts are generally not considered taxable income.

Types of Debts Covered and Not Covered

Debt settlement primarily targets unsecured debts like credit card debt, personal loans, and medical bills. It's generally not suitable for secured debts (like mortgages or car loans) or debts like student loans, child support, or taxes. Bankruptcy, particularly Chapter 7, can discharge most unsecured debts. Chapter 13 can help manage secured debts and catch up on arrears. However, both Chapter 7 and Chapter 13 generally do not discharge student loans (except in very rare cases of undue hardship), recent taxes, child support, or alimony.

Timeframe for Resolution and Financial Recovery

Chapter 7 bankruptcy is typically a quick process, often completed within 3-6 months, providing a relatively fast discharge of debts. Chapter 13 involves a repayment plan lasting 3-5 years. Debt settlement can be a lengthy process, often taking 2-4 years, and there's no guarantee all debts will be settled. While bankruptcy stays on your credit report longer, the immediate discharge of debts can allow you to start rebuilding your credit sooner and more effectively than with unsettled or partially settled debts lingering on your report.

When Debt Settlement Might Be the Better Option Specific Scenarios

While bankruptcy offers a more comprehensive solution, there are specific situations where debt settlement might be a more appealing or appropriate choice:

You Have a Small Number of Debts or Specific Creditors

If you only have a few credit card accounts or specific unsecured debts that are causing you trouble, debt settlement might be manageable. It can be easier to negotiate with a limited number of creditors. If you have a good relationship with a particular creditor or they have a history of settling, this could be a viable path.

You Have Assets You Want to Protect from Liquidation

If you have significant non-exempt assets that you absolutely want to protect and you don't qualify for Chapter 13, debt settlement might be considered. However, it's important to remember that creditors can still sue you and potentially place liens on your assets if they win a judgment, so this protection is not absolute.

You Do Not Qualify for Chapter 7 Bankruptcy

If your income is too high to pass the Chapter 7 means test, and Chapter 13 is not a desirable option for you (perhaps due to the long repayment plan or the types of debts you have), debt settlement could be an alternative. However, carefully weigh the pros and cons, especially the lack of legal protection from creditors.

You Are Concerned About the Stigma of Bankruptcy

For some individuals, the perceived stigma of bankruptcy is a significant deterrent. While both options negatively impact credit, debt settlement is not a public court record in the same way bankruptcy is. If avoiding the 'bankruptcy' label is a top priority, and you understand the risks involved, debt settlement might be considered.

You Can Afford a Lump Sum Payment or Consistent Payments to a Settlement Fund

Debt settlement works best when you have access to a lump sum of money (e.g., from a bonus, inheritance, or sale of an asset) or can consistently make payments into a settlement fund. The ability to offer a significant lump sum often gives you more leverage in negotiations.

When Bankruptcy Might Be the Better Option Critical Situations

For many individuals facing severe financial distress, bankruptcy offers a more robust and legally protected path to a fresh start:

You Have Overwhelming Debt Across Multiple Creditors

If you have a large amount of debt spread across numerous credit cards, personal loans, and medical bills, bankruptcy (especially Chapter 7) can provide a comprehensive discharge of most of these debts. Trying to settle with multiple creditors individually can be an incredibly complex, time-consuming, and often unsuccessful endeavor.

You Are Facing Lawsuits, Wage Garnishments, or Foreclosure

The automatic stay in bankruptcy is a powerful tool that immediately halts most collection actions. If you are being sued, your wages are being garnished, or your home is facing foreclosure, bankruptcy can provide immediate relief and a chance to reorganize or discharge those debts. Debt settlement offers no such immediate legal protection.

You Have Little to No Non-Exempt Assets

For the vast majority of Chapter 7 filers, all their assets are protected by state and federal exemption laws. If you have limited assets that fall within these exemptions, Chapter 7 can discharge your debts without you losing any property, offering a true fresh start.

You Have a Low Income and Cannot Afford to Repay Your Debts

If your income is low and you genuinely cannot afford to make significant payments towards your debts, Chapter 7 bankruptcy is designed for you. It provides a way to eliminate debts when repayment is simply not feasible.

You Need a Quick Resolution and Legal Protection

Chapter 7 bankruptcy offers a relatively fast resolution (3-6 months) and immediate legal protection from creditors. If you need to stop collection activities quickly and get a fresh start, bankruptcy is often the more effective option.

You Have Significant Taxable Debt Forgiveness Concerns

If the potential tax liability from debt settlement is a major concern, bankruptcy eliminates this issue as discharged debts are generally not considered taxable income.

Real-World Examples and Product Comparisons for Debt Relief

Let's look at some hypothetical scenarios and how different debt relief options, including specific products or services, might apply.

Scenario 1 Sarah's Credit Card Crisis

Sarah, a 35-year-old marketing professional, has accumulated $40,000 in credit card debt across five different cards due to a period of unemployment and unexpected medical expenses. She's now back to work, earning $60,000 annually, but her minimum payments are over $1,200 per month, which she can barely afford. She has a modest 401(k) and a car with some equity, but no other significant assets.

Debt Settlement Approach for Sarah

Sarah could approach a debt settlement company like Freedom Debt Relief or National Debt Relief. These companies would advise her to stop paying her credit card companies and instead deposit a monthly amount (e.g., $600-$800) into a dedicated savings account. Over 2-4 years, they would negotiate with her creditors. If they settle for 50% of the debt, she'd pay $20,000 plus their fees (e.g., 20% of $40,000 = $8,000), totaling $28,000. This would be a significant saving compared to $40,000 plus interest. However, her credit score would plummet, she'd face collection calls, and the $20,000 forgiven debt would likely be taxable income.

Bankruptcy Approach for Sarah

Given her income, Sarah might qualify for Chapter 7. If she passes the means test, she could file for Chapter 7. Her 401(k) and car equity would likely be protected by exemptions. Her $40,000 in credit card debt would be discharged within 3-6 months. She would get immediate relief from collection calls. While her credit score would take a hit (a Chapter 7 stays on her report for 10 years), she would be debt-free much faster and without the tax implications of debt settlement. She could then immediately begin rebuilding her credit.

Comparison for Sarah

For Sarah, Chapter 7 bankruptcy appears to be the more advantageous option. It offers a faster, more comprehensive discharge of debt, immediate protection from creditors, and avoids the potential tax bomb of debt settlement. While the credit impact is severe, it's a clean break that allows for quicker credit rebuilding post-discharge.

Scenario 2 Mark's Mortgage and Credit Card Woes

Mark, a 50-year-old small business owner, has $30,000 in credit card debt and is three months behind on his $200,000 mortgage. His business income is inconsistent but generally above the median for his state, making Chapter 7 difficult. He wants to save his home.

Debt Settlement Approach for Mark

Mark could attempt to settle his credit card debt. However, debt settlement would not help him with his mortgage arrears. He would still need to find a way to catch up on his mortgage payments, and the negative credit impact from settling his credit cards could make it harder to refinance or get other financial assistance for his home.

Bankruptcy Approach for Mark

Chapter 13 bankruptcy would be a strong option for Mark. He could propose a repayment plan that includes catching up on his mortgage arrears over 3-5 years, preventing foreclosure. His credit card debt could also be included in the plan, potentially paying back only a fraction of what he owes, without interest. He would keep his home and his business assets. The automatic stay would immediately stop any foreclosure proceedings.

Comparison for Mark

Chapter 13 bankruptcy is clearly superior for Mark. It addresses both his credit card debt and, crucially, allows him to save his home from foreclosure, which debt settlement cannot do. The structured repayment plan provides a clear path to financial stability.

Scenario 3 Lisa's Small Debt Load and Good Income

Lisa, a 28-year-old with a stable job earning $75,000, has $10,000 in credit card debt from a past emergency. She can afford to pay it off but wants to reduce the total amount. She has excellent credit otherwise and is very concerned about maintaining it.

Debt Settlement Approach for Lisa

Lisa could try to negotiate directly with her credit card company for a settlement, or use a service like CuraDebt (which offers both debt settlement and debt consolidation). If she settles for $6,000, she saves $4,000. However, her credit score would still be negatively impacted by the 'settled for less than full amount' mark, which would stay on her report for seven years. The $4,000 forgiven debt would be taxable income.

Bankruptcy Approach for Lisa

Given her income and relatively small debt, Lisa would likely not qualify for Chapter 7. Chapter 13 would involve a 3-5 year repayment plan for $10,000, which might not be worth the effort and cost compared to simply paying off the debt. Filing bankruptcy for $10,000 in debt, especially with a good income, is generally not advisable due to the severe and long-lasting credit impact.

Comparison for Lisa

For Lisa, neither debt settlement nor bankruptcy is ideal. Her best option might be a debt consolidation loan (if her credit is still good enough) or a structured debt management plan through a non-profit credit counseling agency like the National Foundation for Credit Counseling (NFCC). These options would help her pay off the debt in full, potentially at a lower interest rate, without the severe credit damage or tax implications of settlement or bankruptcy. If she insists on reducing the principal, direct negotiation with the creditor might be her best bet, accepting the credit hit as a trade-off.

Choosing Your Path Forward Expert Advice and Resources

Deciding between debt settlement and bankruptcy is a deeply personal and complex choice. It's not a one-size-fits-all situation. The best option depends on the amount and type of your debt, your income, your assets, your long-term financial goals, and your tolerance for risk and credit damage.

Consult with a Qualified Professional

Before making any decision, it is highly recommended to consult with both a qualified bankruptcy attorney and a reputable non-profit credit counselor. A bankruptcy attorney can assess your eligibility for Chapter 7 or Chapter 13, explain the legal process, and advise you on the potential outcomes and costs. A credit counselor can review your entire financial situation, explore all available debt relief options (including debt management plans, debt consolidation, and budgeting), and help you understand the implications of each. They can provide unbiased advice, as they are not incentivized to push one solution over another.

Key Questions to Ask Yourself

- How much debt do I have, and what types of debt are they (secured vs. unsecured)?

- What is my current income, and is it stable?

- What assets do I own, and are they protected by exemptions?

- Am I facing lawsuits, wage garnishments, or foreclosure?

- How important is my credit score to me in the short term vs. long term?

- Can I realistically afford to make consistent payments towards a debt settlement fund?

- Am I comfortable with the potential tax implications of debt settlement?

- What are my long-term financial goals?

Reputable Resources and Products for Debt Relief

When seeking help, always look for reputable organizations. For credit counseling and debt management plans, consider:

- National Foundation for Credit Counseling (NFCC): A non-profit organization that provides free or low-cost credit counseling and debt management plans. They have a network of certified counselors across the country.

- Financial Counseling Association of America (FCAA): Another non-profit organization offering similar services.

For debt settlement, if you decide it's the right path, research companies thoroughly. Look for those with a strong track record, transparent fees, and positive reviews. Be wary of companies that guarantee results or pressure you into signing up. Some well-known names include:

- Freedom Debt Relief: One of the largest debt settlement companies, offering negotiation services for unsecured debts.

- National Debt Relief: Another prominent company in the debt settlement space, known for its negotiation services.

- CuraDebt: Offers both debt settlement and tax debt relief services.

For bankruptcy, always consult with a local, experienced bankruptcy attorney. Websites like the National Association of Consumer Bankruptcy Attorneys (NACBA) can help you find qualified lawyers in your area.

Ultimately, the choice between debt settlement and bankruptcy is about weighing the severity of your debt, your ability to repay, the impact on your credit, and your desire for a fresh start. Both are serious financial tools, and understanding their nuances is the first step toward regaining control of your financial life. Take your time, gather all the facts, and seek professional guidance to make the decision that is truly best for you.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)