Secured Credit Cards Best for Building Credit

Compare the best secured credit cards designed to help you build or rebuild your credit history effectively.

Compare the best secured credit cards designed to help you build or rebuild your credit history effectively.

Secured Credit Cards Best for Building Credit

Hey there! Are you looking to build or rebuild your credit? Maybe you're just starting out, or perhaps you've had a few financial bumps in the road. Whatever your situation, a secured credit card can be a fantastic tool to help you establish a positive credit history. Unlike traditional unsecured credit cards, secured cards require a security deposit, which typically acts as your credit limit. This deposit minimizes risk for the issuer, making them more accessible to individuals with limited or poor credit. Think of it as a stepping stone to better financial health. In this comprehensive guide, we're going to dive deep into the world of secured credit cards, exploring how they work, who they're best for, and most importantly, recommending some of the top options available in the US and Southeast Asian markets. We'll also compare their features, fees, and even give you an idea of their typical costs.

What is a Secured Credit Card and How Does it Work for Credit Building?

Let's break down the basics. A secured credit card is a type of credit card that's backed by a cash deposit you make to the issuing bank. This deposit usually equals your credit limit. For example, if you deposit $300, your credit limit will be $300. This deposit serves as collateral, reducing the risk for the lender. Because of this reduced risk, secured cards are much easier to get approved for, even if you have no credit history or a less-than-perfect one. When you use a secured card, it works just like a regular credit card: you make purchases, and you receive a monthly statement. The key difference is that if you fail to pay your bill, the issuer can use your security deposit to cover the debt. But here's the good news: as long as you make your payments on time and keep your credit utilization low (ideally below 30% of your limit), the card issuer will report your positive payment activity to the major credit bureaus. This consistent reporting is what helps you build a strong credit history over time. After a period of responsible use, typically 6 to 18 months, many secured card issuers will review your account and may offer to convert your card to an unsecured one, or even return your deposit. This transition is a clear sign that you've successfully built your credit!

Who Should Consider a Secured Credit Card for Credit Improvement?

Secured credit cards aren't for everyone, but they're a perfect fit for several groups of people:

- Credit Newbies: If you're fresh out of college, new to the country, or simply haven't had a credit card before, a secured card is an excellent way to establish your first credit file.

- Credit Rebuilders: For those who've faced bankruptcy, foreclosures, or other financial setbacks, a secured card offers a second chance to demonstrate responsible credit behavior and repair damaged credit scores.

- Budget-Conscious Spenders: Because your credit limit is tied to your deposit, secured cards can help prevent overspending, making them a good choice for individuals who want to practice responsible credit habits.

- Those Denied Unsecured Cards: If you've applied for traditional credit cards and been rejected due to your credit history, a secured card is often the next logical step.

Key Features to Look for in the Best Secured Credit Cards for Building Credit

When you're shopping for a secured credit card, not all cards are created equal. Here are some crucial features to prioritize:

- Reporting to All Three Major Credit Bureaus: This is non-negotiable. Ensure the card reports your payment activity to Equifax, Experian, and TransUnion. This is how your credit score improves.

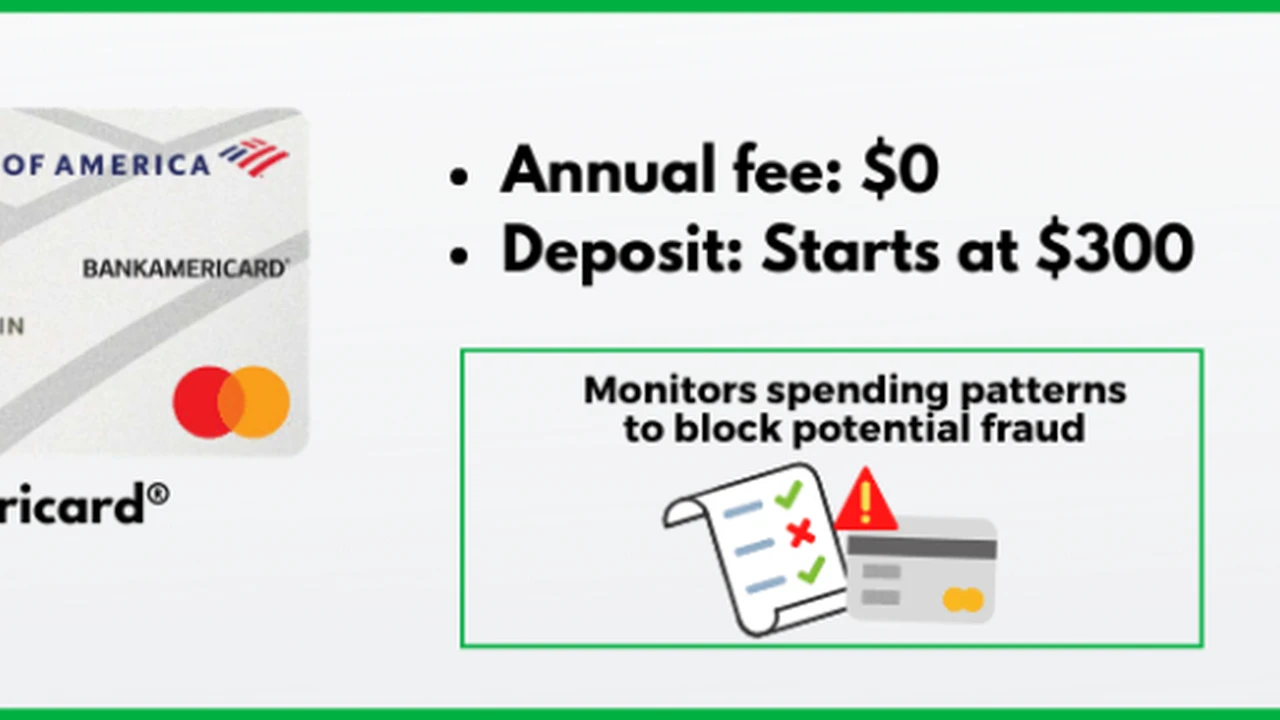

- Low or No Annual Fee: While some secured cards have annual fees, aim for those with lower fees or none at all to maximize your savings.

- Path to Unsecured Card: Many of the best secured cards offer a clear path to upgrading to an unsecured card and getting your deposit back after a period of responsible use. This is a huge plus!

- Flexible Security Deposit Options: Look for cards that allow you to choose your deposit amount, giving you control over your credit limit. Some even allow you to add to your deposit over time.

- Credit Limit Increases: Some cards offer automatic credit limit increases without requiring an additional deposit, which can further boost your credit score.

- No Hard Credit Check for Application: While less common, some secured cards might not perform a hard credit inquiry, which can be beneficial if you're trying to avoid further dings to your credit score.

- Rewards Programs: While not the primary focus, some secured cards offer modest rewards, like cash back, which can be a nice bonus.

Top Secured Credit Cards for Credit Building in the US Market

Let's dive into some of the best secured credit card options available in the United States, comparing their features, typical usage scenarios, and estimated costs.

Discover it Secured Credit Card A Top Choice for Rewards and Upgrade Path

Why it's great: The Discover it Secured Card is consistently ranked as one of the best secured cards, and for good reason. It offers cash back rewards, which is rare for a secured card, and has a clear path to transitioning to an unsecured card. Discover is also known for its excellent customer service.

- Key Features:

- 1% cash back on all purchases, 2% cash back at gas stations and restaurants (on up to $1,000 in combined purchases each quarter).

- Discover matches all the cash back you've earned at the end of your first year, automatically.

- No annual fee.

- Reports to all three major credit bureaus.

- Regular account reviews starting at 7 months to see if you qualify for an unsecured card and get your deposit back.

- Free FICO Score access.

- Typical Usage Scenario: Perfect for individuals who want to earn rewards while building credit and are committed to responsible spending. It's a great stepping stone to a full-fledged Discover unsecured card.

- Security Deposit: Minimum $200, maximum $2,500.

- Estimated Cost: No annual fee. APR typically ranges from 24.99% to 28.99% Variable.

Capital One Platinum Secured Credit Card Easy Approval and Upgrade Potential

Why it's great: The Capital One Platinum Secured Card is known for its relatively easy approval process and flexible security deposit options. It's a solid choice for those with very limited or poor credit who need a reliable card to start building.

- Key Features:

- No annual fee.

- Reports to all three major credit bureaus.

- Potential for a lower security deposit ($49, $99, or $200) for a $200 credit line, depending on your creditworthiness.

- Automatic credit line reviews in as little as 6 months, with the possibility of getting your deposit back and upgrading to an unsecured card.

- Access to Capital One's credit education tools.

- Typical Usage Scenario: Ideal for those with very poor or no credit who might struggle to get approved elsewhere. The lower initial deposit option can be a significant advantage.

- Security Deposit: $49, $99, or $200 for a $200 credit line. You can deposit more for a higher credit line.

- Estimated Cost: No annual fee. APR typically around 29.99% Variable.

Chime Credit Builder Visa Secured Card No Credit Check and No Fees

Why it's great: The Chime Credit Builder Card stands out because it requires no credit check to apply and has no annual fee or interest. It's unique in that your security deposit isn't a fixed amount; instead, you move money from your Chime Checking Account into your Credit Builder Secured Account, and that amount becomes your credit limit. This gives you incredible control.

- Key Features:

- No annual fee, no interest, no credit check to apply.

- Reports to all three major credit bureaus.

- Your credit limit is determined by the amount of money you move into your Credit Builder Secured Account.

- Uses a unique 'Safer Credit Building' feature where you can only spend what you've moved into the account, preventing debt.

- Requires a Chime Checking Account with a qualifying direct deposit of $200 or more.

- Typical Usage Scenario: Best for individuals who already use Chime for their banking or are willing to switch. It's an excellent option for those who want to build credit without the risk of accumulating debt or paying interest.

- Security Deposit: Flexible, determined by the amount you move from your Chime Checking Account.

- Estimated Cost: No annual fee, no interest.

OpenSky Secured Visa Credit Card No Credit Check Required

Why it's great: The OpenSky Secured Visa is another excellent option for those with poor or no credit because it doesn't require a credit check for approval. This makes it highly accessible, though it does come with an annual fee.

- Key Features:

- No credit check required for approval.

- Reports to all three major credit bureaus.

- Choose your own credit limit from $200 to $3,000, based on your security deposit.

- Online credit education resources.

- Typical Usage Scenario: Ideal for individuals who have been denied other secured cards due to past credit issues and need a guaranteed approval option.

- Security Deposit: Minimum $200, maximum $3,000.

- Estimated Cost: $35 annual fee. APR typically around 25.64% Variable.

Top Secured Credit Cards for Credit Building in the Southeast Asian Market

The secured credit card landscape in Southeast Asia can vary significantly by country, with different banks offering different products. However, the core concept remains the same. Here are some general types of secured cards you might find and examples from prominent banks in the region. Keep in mind that specific product names and features can change, so always check with local banks.

General Features of Secured Cards in Southeast Asia for Credit Building

In countries like Singapore, Malaysia, Thailand, Indonesia, and the Philippines, secured credit cards are often referred to as 'deposit-backed credit cards' or 'secured credit cards against fixed deposit.' They typically work by linking your credit limit to a fixed deposit account you hold with the bank.

- Fixed Deposit as Collateral: The most common model involves placing a fixed deposit with the bank, and your credit limit is a percentage of that deposit (e.g., 80-100%).

- Reporting to Local Credit Bureaus: Ensure the card reports to the relevant credit bureaus in your country (e.g., Credit Bureau Singapore, CTOS/Experian in Malaysia, National Credit Bureau in Thailand, Credit Information Corporation in the Philippines).

- Annual Fees: Many secured cards in this region will have an annual fee, though some may waive it for the first year.

- Interest Rates: Interest rates can be quite high, so paying your balance in full is crucial.

- Upgrade Path: While not always explicitly advertised, demonstrating responsible use can often lead to an upgrade to an unsecured card or a higher credit limit.

Example: DBS/POSB Secured Credit Cards (Singapore) Building Credit with a Local Giant

DBS and POSB are major banks in Singapore, and they offer secured credit card options. These are typically linked to a fixed deposit account.

- Key Features (General):

- Credit limit usually 80-100% of your fixed deposit amount.

- Reports to Credit Bureau Singapore (CBS).

- Standard credit card features like online banking, mobile app access.

- Often available to non-residents with a valid work pass and fixed deposit.

- Typical Usage Scenario: Excellent for new residents, young professionals, or those rebuilding credit in Singapore. It leverages the trust and widespread acceptance of a major local bank.

- Security Deposit: Varies, typically starting from S$1,000 or S$2,000 for a fixed deposit.

- Estimated Cost: Annual fee (e.g., S$192.60 for some cards, often waived for the first year). APR typically around 26.9% p.a.

Example: Maybank Secured Credit Cards (Malaysia) Accessible Credit Building

Maybank, a leading bank in Malaysia, also provides secured credit card options, often tied to a fixed deposit or savings account.

- Key Features (General):

- Credit limit often 80-100% of the pledged deposit.

- Reports to CTOS and Experian (Malaysia's credit bureaus).

- May offer basic rewards or benefits depending on the specific card product.

- Typical Usage Scenario: Suitable for Malaysians or long-term residents looking to establish or improve their credit score within the local banking system.

- Security Deposit: Varies, often starting from RM1,000 or RM2,000.

- Estimated Cost: Annual fee (e.g., RM80-RM100 for some cards, potentially waived with spending). APR typically around 15-18% p.a.

Example: BDO Secured Credit Cards (Philippines) Building Credit with a Major Player

BDO Unibank, one of the largest banks in the Philippines, offers secured credit card products, usually linked to a hold-out deposit.

- Key Features (General):

- Credit limit typically 80-90% of the hold-out deposit.

- Reports to the Credit Information Corporation (CIC).

- Access to BDO's extensive branch network and online services.

- Typical Usage Scenario: Great for Filipinos or foreign residents in the Philippines who need a reliable way to build credit with a widely accepted card.

- Security Deposit: Varies, often starting from PHP10,000 to PHP25,000.

- Estimated Cost: Annual fee (e.g., PHP1,500-PHP2,500, sometimes waived for the first year). APR typically around 3% per month.

Comparing Secured Credit Cards Key Considerations for Your Choice

When you're weighing your options, here's a quick comparison checklist:

- Annual Fee: Is there one? How much is it? Can it be waived?

- Security Deposit: What's the minimum and maximum? Is it flexible?

- APR: What's the interest rate? Remember, you should aim to pay in full to avoid interest.

- Credit Bureau Reporting: Does it report to all relevant bureaus (three in the US, local bureaus in SEA)?

- Upgrade Path: Is there a clear path to an unsecured card and getting your deposit back?

- Rewards: Are there any rewards? (A bonus, but not the main goal for credit building).

- Customer Service: How is the issuer's customer service reputation?

- Additional Features: Free credit score access, credit education tools, etc.

Tips for Maximizing Your Credit Building with a Secured Card

Getting a secured card is just the first step. To truly make it work for you, follow these best practices:

- Pay Your Bill On Time, Every Time: This is the single most important factor in building good credit. Set up automatic payments if you can.

- Keep Your Credit Utilization Low: Try to keep your spending below 30% of your credit limit. For example, if your limit is $300, try not to spend more than $90. Lower is even better!

- Don't Close Old Accounts: Once you get your deposit back or upgrade to an unsecured card, don't immediately close your secured card (if it converts). Older accounts contribute positively to your credit history length.

- Monitor Your Credit Report: Regularly check your credit report for errors. You can get free copies annually from AnnualCreditReport.com in the US, and local bureaus in SEA often offer similar services.

- Be Patient: Building credit takes time. Stick with responsible habits, and you'll see results.

Potential Downsides and How to Mitigate Them for Credit Building

While secured cards are fantastic tools, they do have a few potential drawbacks:

- Security Deposit Requirement: This can be a barrier for some, as you need to have the cash upfront. Mitigation: Look for cards with lower minimum deposits or flexible deposit options.

- Annual Fees: Some secured cards charge annual fees, which eat into your budget. Mitigation: Prioritize cards with no annual fee or very low fees.

- High APR: Interest rates on secured cards can be high. Mitigation: Always pay your balance in full every month to avoid paying any interest.

- No Rewards: Many secured cards don't offer rewards. Mitigation: If rewards are important, consider the Discover it Secured Card or other rare options that do.

The Journey from Secured to Unsecured Credit for Financial Growth

The ultimate goal of using a secured credit card is to eventually qualify for an unsecured card. This transition signifies that you've demonstrated responsible credit behavior and are now trusted by lenders without needing collateral. Many secured card issuers will automatically review your account after a certain period (e.g., 6-12 months) of on-time payments and low utilization. If you meet their criteria, they might:

- Upgrade your card: Convert your secured card to an unsecured version of the same card, returning your deposit.

- Offer a new unsecured card: Invite you to apply for one of their unsecured products, returning your deposit from the secured card.

Even if your current issuer doesn't offer an automatic upgrade, your improved credit score will make you eligible for a wider range of unsecured cards from other lenders. When this happens, you can apply for a new unsecured card, and once approved, close your secured card account and get your deposit back. Just remember to keep that old account open for a while if it's reporting positively, as account age is a factor in your credit score.

Final Thoughts on Secured Credit Cards for Credit Building

Secured credit cards are powerful instruments for anyone looking to build or rebuild their credit. They offer a safe and structured way to demonstrate financial responsibility to lenders. By choosing the right card, making timely payments, and keeping your utilization low, you can effectively use a secured card as a springboard to a healthier credit score and a brighter financial future. Whether you're in the US or Southeast Asia, there are options available to help you on your credit journey. Do your research, compare the features, and commit to responsible credit habits. You've got this!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)