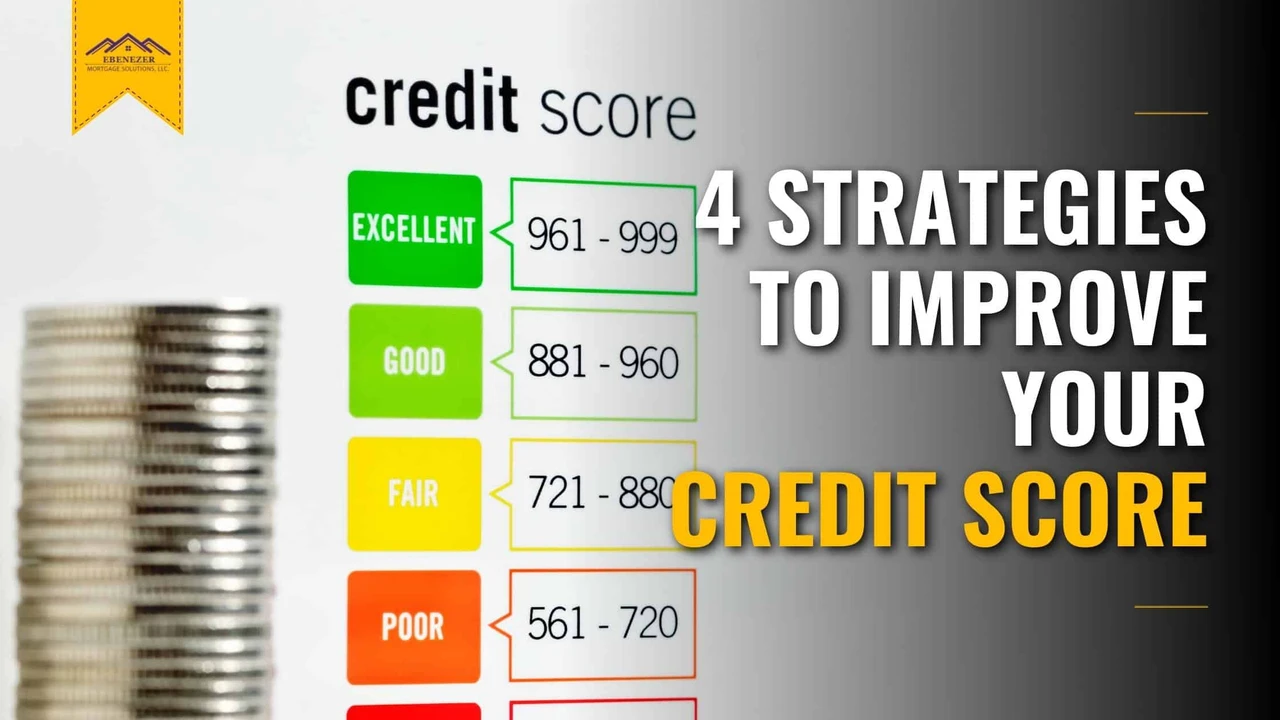

Improving Your Credit Score Fast 10 Strategies

Discover 10 effective strategies to quickly improve your credit score and unlock better lending opportunities.

Discover 10 effective strategies to quickly improve your credit score and unlock better lending opportunities.

Improving Your Credit Score Fast 10 Strategies

Hey there! Looking to give your credit score a quick boost? You're in the right place. A good credit score isn't just a number; it's your financial passport to better interest rates on loans, easier approvals for apartments, and even lower insurance premiums. Whether you're eyeing a new car, a home, or just want to improve your financial standing, getting your credit score up can make a huge difference. We're talking about practical, actionable steps you can take right now to see some positive movement. Forget the magic bullet – credit repair takes effort, but with these 10 strategies, you'll be well on your way to a healthier financial future. Let's dive in!

Strategy 1 Address Credit Report Errors Your First Line of Defense

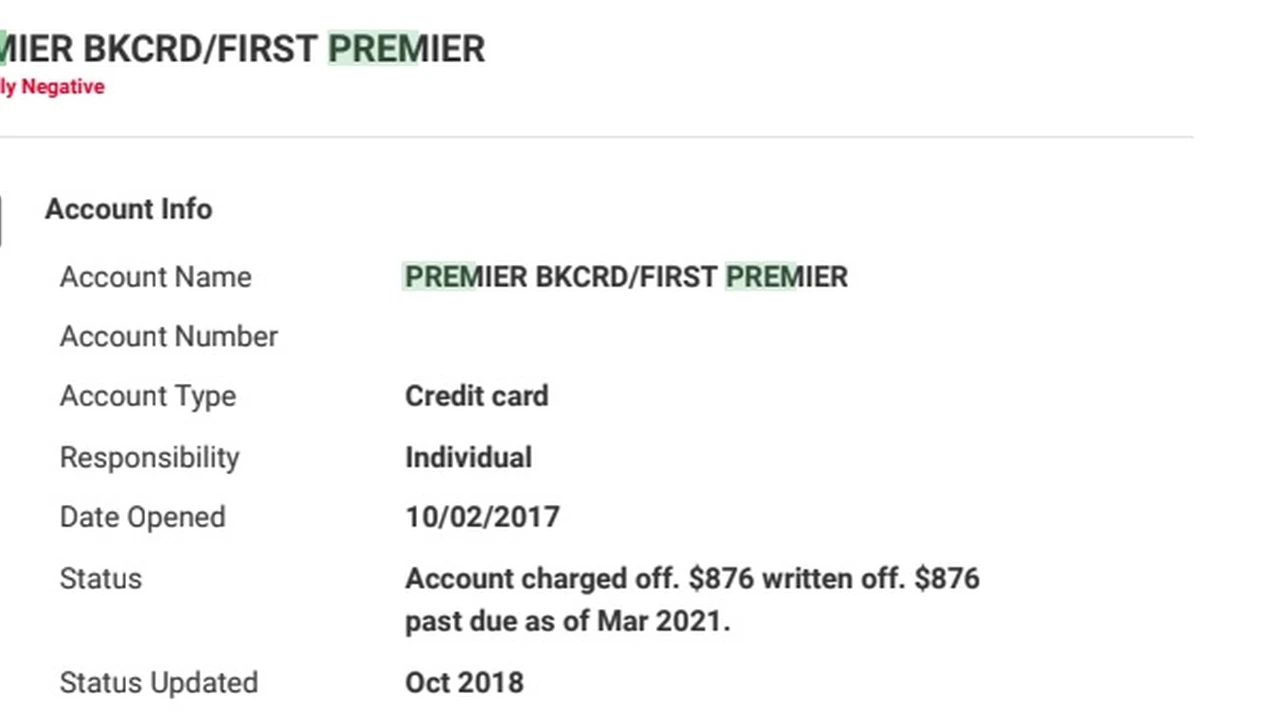

One of the quickest and most impactful ways to improve your credit score is by cleaning up your credit report. Believe it or not, errors are more common than you think. These could be anything from incorrect account balances to accounts that don't even belong to you. These mistakes can drag your score down significantly. So, what's the game plan?

How to Find and Dispute Credit Report Errors

First things first, you need to get copies of your credit reports from all three major credit bureaus: Experian, Equifax, and TransUnion. You can do this for free once a year at AnnualCreditReport.com. Don't just skim them; go through every single entry with a fine-tooth comb. Look for:

- Incorrect personal information: Wrong name, address, or Social Security number.

- Accounts that aren't yours: This could be a sign of identity theft.

- Incorrect account status: An account marked as open when it's closed, or vice versa.

- Late payments that were actually on time: A common error that can severely impact your score.

- Duplicate accounts: The same debt listed multiple times.

- Incorrect balances or credit limits: These can affect your credit utilization.

Once you spot an error, you need to dispute it. You can do this directly with the credit bureau online, by mail, or by phone. Provide as much documentation as possible to support your claim. The credit bureau has 30-45 days to investigate and respond. If they find an error, they must correct it, and you should see your score improve. This step is crucial because it's like removing a heavy anchor from your credit score.

Strategy 2 Tackle Credit Utilization Keep It Low

Your credit utilization ratio is a huge factor in your credit score, accounting for about 30% of your FICO score. This ratio is calculated by dividing your total credit card balances by your total credit limits. Lenders like to see this number low, ideally below 30%. The lower, the better, with under 10% being excellent.

Practical Steps to Reduce Your Credit Utilization

- Pay down balances: This is the most direct way. Focus on cards with high balances first. Even paying a little extra each month can make a difference.

- Make multiple payments: Instead of waiting for your statement, make payments throughout the month. This can keep your reported balance lower.

- Ask for a credit limit increase: If your spending habits are stable and you have a good payment history, asking your credit card company for a higher limit can instantly lower your utilization ratio (assuming you don't increase your spending). Be cautious with this, as a hard inquiry might temporarily ding your score, but the long-term benefit can outweigh it.

- Avoid closing old accounts: While it might seem counterintuitive, closing an old credit card account can actually hurt your utilization by reducing your total available credit.

Strategy 3 Payment History Consistency is Key

Your payment history is the single most important factor in your credit score, making up about 35% of your FICO score. This means paying your bills on time, every time, is non-negotiable for a good credit score. Even one late payment can drop your score by dozens of points and stay on your report for up to seven years.

How to Ensure On-Time Payments

- Set up automatic payments: This is a no-brainer. Most banks and credit card companies offer this feature. Just make sure you have enough funds in your account to cover the payments.

- Set reminders: Use calendar alerts, phone reminders, or even sticky notes to remind yourself a few days before a payment is due.

- Adjust due dates: If your paychecks come in at a specific time, call your creditors and ask to adjust your due dates to align with your income.

- Pay more than the minimum: While paying on time is crucial, paying more than the minimum due helps reduce your balance faster, which in turn helps your utilization and saves you money on interest.

Strategy 4 Become an Authorized User Boost Your Score with Help

If you have a trusted family member or friend with excellent credit and a long, positive payment history, becoming an authorized user on one of their credit cards can be a quick way to piggyback on their good credit. When you're added as an authorized user, that account's history (including its low utilization and on-time payments) can appear on your credit report, potentially boosting your score.

Considerations for Authorized User Status

- Choose wisely: Make sure the primary cardholder is financially responsible. Their mistakes can become your mistakes.

- Discuss expectations: Clarify whether you'll actually use the card or if it's purely for credit-building purposes.

- Not all lenders report: While most do, some credit card companies don't report authorized user activity to all three bureaus.

Strategy 5 Get a Secured Credit Card A Stepping Stone to Better Credit

If your credit is poor or you have no credit history, a secured credit card can be a fantastic tool. Unlike traditional credit cards, secured cards require a cash deposit, which typically becomes your credit limit. This deposit acts as collateral, reducing the risk for the lender. As you use the card responsibly and make on-time payments, the issuer reports your activity to the credit bureaus, helping you build a positive payment history.

Top Secured Credit Card Options

When looking for a secured credit card, consider factors like annual fees, interest rates, and whether the card graduates to an unsecured card. Here are a few popular options:

Discover it Secured Credit Card

- Features: No annual fee, reports to all three major credit bureaus, offers cash back rewards (1% on all purchases, 2% at gas stations and restaurants on up to $1,000 in combined purchases each quarter), and Discover automatically reviews your account after 7 months to see if you can transition to an unsecured card and get your deposit back.

- Use Case: Excellent for those looking to earn rewards while building credit and hoping to graduate to an unsecured card.

- Typical Deposit: $200 - $2,500 (your credit limit).

- Approximate Cost: $0 annual fee.

Capital One Platinum Secured Credit Card

- Features: No annual fee, reports to all three major credit bureaus, and offers a path to a higher credit line after 6 months of on-time payments. Some applicants may qualify for a lower deposit ($49 or $99) for a $200 credit line.

- Use Case: Great for those with very limited or poor credit who need a straightforward card with a low barrier to entry.

- Typical Deposit: $49, $99, or $200 for a $200 credit line.

- Approximate Cost: $0 annual fee.

OpenSky Secured Visa Credit Card

- Features: No credit check required for approval, reports to all three major credit bureaus, and allows you to choose your credit limit based on your deposit.

- Use Case: Ideal for individuals who have been denied other secured cards due to past credit issues, as it doesn't require a credit check.

- Typical Deposit: $200 - $3,000.

- Approximate Cost: $35 annual fee.

Strategy 6 Consider a Credit Builder Loan A Unique Approach

A credit builder loan is a bit different from a traditional loan. Instead of receiving the money upfront, the loan amount is held in a savings account or CD while you make monthly payments. Once the loan is fully paid off, you receive the money. The lender reports your on-time payments to the credit bureaus, helping you build a positive payment history and improve your score. It's essentially a forced savings plan that also builds credit.

Popular Credit Builder Loan Providers

These loans are often offered by credit unions and community banks, but some online platforms specialize in them:

Self Credit Builder Account

- Features: Offers various loan amounts and terms, reports to all three major credit bureaus, and once the loan is paid off, you get access to the funds. They also offer a secured credit card option after a few months of on-time payments.

- Use Case: Excellent for those who want a structured way to save money and build credit simultaneously.

- Typical Loan Amounts: $500 - $2,000.

- Approximate Cost: Administrative fee (e.g., $9) and interest on the loan (e.g., 15.92% APR).

Kikoff Credit Account

- Features: A unique credit-building product that gives you a $750 credit line to use exclusively in the Kikoff store. You make small monthly payments (e.g., $10) on purchases, and these payments are reported to Equifax and Experian. No hard credit check.

- Use Case: Good for those looking for a very low-cost, low-commitment way to add a tradeline to their credit report.

- Typical Credit Line: $750.

- Approximate Cost: $5 per month for the credit account.

Credit Strong Credit Builder Loan

- Features: Offers various loan sizes and terms, reports to all three major credit bureaus, and allows you to build savings while building credit.

- Use Case: Suitable for those who want more flexibility in loan amounts and terms, and a clear path to building savings.

- Typical Loan Amounts: $1,000 - $25,000.

- Approximate Cost: Monthly payments vary based on loan amount and term, with interest rates around 10-15%.

Strategy 7 Pay Down High-Interest Debt Prioritize Smartly

While all debt impacts your credit utilization, high-interest debt, especially on credit cards, can be a major drain on your finances and make it harder to pay down balances. By strategically paying off these debts, you not only save money on interest but also free up cash flow to tackle other financial goals, including further credit improvement.

Debt Payoff Methods to Consider

- Debt Avalanche: Focus on paying off the debt with the highest interest rate first, while making minimum payments on others. Once that's paid, roll the money you were paying into the next highest interest debt. This method saves you the most money on interest.

- Debt Snowball: Focus on paying off the smallest debt first, while making minimum payments on others. Once that's paid, roll the money into the next smallest debt. This method provides psychological wins, keeping you motivated.

Choose the method that best suits your personality and financial situation. Both are effective for reducing debt and improving your credit utilization.

Strategy 8 Keep Old Accounts Open Maintain Credit History Length

The length of your credit history (how long you've had credit accounts open) accounts for about 15% of your FICO score. Closing old, unused credit card accounts might seem like a good idea to simplify your finances, but it can actually hurt your score. When you close an old account, you reduce your average age of accounts and potentially decrease your total available credit, which can negatively impact your credit utilization.

When to Keep or Close Accounts

- Keep open: If an old account has no annual fee and a good payment history, it's generally best to keep it open, even if you rarely use it. Consider making a small purchase every few months and paying it off immediately to keep it active.

- Consider closing: If an old account has a high annual fee and you don't use it, or if it's tempting you to overspend, then closing it might be worth the potential temporary dip in your score for the long-term financial benefit.

Strategy 9 Mix Up Your Credit Types Diversify Your Portfolio

Having a healthy mix of credit accounts (e.g., credit cards, installment loans like car loans or mortgages) can positively impact your credit score, accounting for about 10% of your FICO score. Lenders like to see that you can responsibly manage different types of credit. However, this doesn't mean you should take out loans you don't need just to diversify your credit mix.

Smart Credit Mix Strategies

- Natural progression: As you go through life, you'll naturally acquire different types of credit (student loans, car loans, a mortgage). Managing these responsibly will build a diverse credit profile.

- Avoid unnecessary debt: Only take on new credit if you genuinely need it and can afford the payments. The goal is to show responsible management, not just to have more accounts.

Strategy 10 Monitor Your Credit Regularly Stay Informed

Regularly checking your credit report and score is not just about finding errors; it's about staying informed and proactive. Monitoring helps you spot potential identity theft early, track your progress, and understand how your financial actions impact your score. Many services offer free credit monitoring, and some credit card companies provide free FICO or VantageScore access.

Recommended Credit Monitoring Tools

There are several excellent tools available to help you keep an eye on your credit:

Credit Karma

- Features: Provides free VantageScore 3.0 scores from TransUnion and Equifax, along with credit reports. Offers insights into factors affecting your score and personalized recommendations.

- Use Case: Great for general credit monitoring, understanding score changes, and getting personalized advice.

- Approximate Cost: Free.

Experian Free Credit Report and FICO Score

- Features: Offers a free Experian FICO Score 8, along with your Experian credit report. You can also get free credit monitoring and alerts.

- Use Case: Essential for tracking your FICO score, which is widely used by lenders, and monitoring your Experian report.

- Approximate Cost: Free.

MyFICO

- Features: Provides access to all three bureau credit reports and FICO scores (including various industry-specific FICO scores). Offers comprehensive credit monitoring and alerts.

- Use Case: Best for those who want the most detailed and accurate FICO score information, especially if applying for a mortgage or other major loans.

- Approximate Cost: Paid subscription plans (e.g., $19.95/month for basic, $39.95/month for premium).

By consistently applying these 10 strategies, you'll be well on your way to a significantly improved credit score. Remember, it's a marathon, not a sprint, but every positive step you take builds momentum. Good luck on your credit-building journey!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)