Investing for Beginners Top 5 Tips

A comprehensive guide to financial planning for young adults covering budgeting, saving, and investing.

A comprehensive guide to financial planning for young adults covering budgeting, saving, and investing.

Financial Planning for Young Adults Essential Guide

Hey there, future financial rockstars! Are you just starting out in your career, navigating college life, or perhaps trying to figure out what 'adulting' even means when it comes to money? You're in the right place! Financial planning might sound like something your parents or a fancy Wall Street executive does, but trust me, it's for everyone, especially young adults. Getting a handle on your finances early can set you up for a lifetime of success, freedom, and fewer money-related headaches. This isn't about becoming a millionaire overnight; it's about building smart habits, making informed decisions, and understanding how your money can work for you. Let's dive into this essential guide to financial planning for young adults, covering everything from budgeting and saving to smart investing.

Why Financial Planning Matters for Young Adults Your Future Self Will Thank You

You might be thinking, 'I'm young, I have plenty of time to worry about money later.' While it's true you have time, that's precisely why starting now is so powerful. The magic of compound interest, the ability to recover from mistakes, and the sheer peace of mind that comes with financial stability are all amplified when you begin early. Think about it: small, consistent actions today can lead to massive rewards down the road. Avoiding common financial pitfalls, building an emergency fund, and understanding how to invest even small amounts can make a monumental difference. This isn't just about saving for a rainy day; it's about building the foundation for your dream life, whether that's buying a home, traveling the world, or retiring comfortably.

Budgeting Basics for Young Adults Taking Control of Your Cash Flow

Budgeting isn't about restricting yourself; it's about empowering yourself. It's a tool to understand where your money is going so you can direct it towards your goals. For young adults, this often means balancing student loan payments, rent, social activities, and maybe even a first car payment. It can feel overwhelming, but a simple budget can bring clarity.

The 50/30/20 Rule A Simple Budgeting Framework

One of the easiest budgeting methods to start with is the 50/30/20 rule:

- 50% for Needs: This includes essentials like rent/mortgage, utilities, groceries, transportation, insurance, and minimum loan payments.

- 30% for Wants: This is your fun money! Dining out, entertainment, subscriptions, shopping, hobbies, and travel fall into this category.

- 20% for Savings & Debt Repayment: This is crucial for building your emergency fund, retirement savings, and paying down high-interest debt beyond the minimums.

Budgeting Tools and Apps Making it Easy

Gone are the days of complicated spreadsheets (unless you love them!). There are fantastic apps and tools that automate much of the budgeting process. Here are a few popular ones:

- Mint: A free, comprehensive budgeting app that links to your bank accounts, credit cards, and investments. It categorizes transactions, tracks spending, and helps you set budgets. It's great for seeing your entire financial picture in one place.

- You Need A Budget (YNAB): This app follows a 'zero-based budgeting' philosophy, meaning every dollar has a job. It's a bit more hands-on but incredibly effective for gaining granular control over your money. YNAB has a monthly subscription fee but offers a free trial.

- Personal Capital: While more focused on investment tracking, Personal Capital also offers excellent budgeting and net worth tracking features. It's free and provides a holistic view of your finances.

- Fudget: A super simple, no-frills budgeting app for those who just want to track income and expenses without all the bells and whistles. It's free with an optional paid upgrade.

- Good Old Spreadsheet: Don't underestimate the power of a Google Sheet or Excel document. You can customize it exactly to your needs, and there are tons of free templates available online.

Product Comparison:

| Product | Key Feature | Pricing | Best For |

|---|---|---|---|

| Mint | All-in-one financial dashboard, free | Free | Beginners, comprehensive overview |

| YNAB | Zero-based budgeting, active management | $14.99/month or $99/year | Detailed control, debt payoff |

| Personal Capital | Investment focus, net worth tracking | Free (advisory services extra) | High-net-worth individuals, investors |

| Fudget | Simplicity, manual entry | Free (Pro version $4.99 one-time) | Minimalists, basic tracking |

Saving Strategies for Young Adults Building Your Financial Safety Net and Future

Once you have a budget, the next step is to make sure you're actually saving money. Saving isn't just for big purchases; it's for building an emergency fund, saving for a down payment, or even just having a buffer for unexpected expenses. The earlier you start, the less you'll have to save later, thanks to compound interest.

The Emergency Fund Your Financial Shield

This is non-negotiable. An emergency fund is 3-6 months' worth of living expenses saved in an easily accessible, high-yield savings account. This money is for true emergencies: job loss, unexpected medical bills, car repairs, etc. It prevents you from going into debt when life throws a curveball.

High Yield Savings Accounts Maximizing Your Returns

Don't let your emergency fund sit in a regular checking account earning next to nothing. High-yield savings accounts (HYSAs) offer significantly better interest rates. While rates fluctuate, they are consistently higher than traditional banks. Look for online banks, as they often have lower overheads and can pass those savings on to you.

Recommended HYSAs (as of late 2023/early 2024, rates are variable):

- Ally Bank Online Savings Account: Known for competitive rates, no monthly fees, and excellent customer service. They also offer checking accounts and investment options, making it easy to keep all your money in one place.

- Marcus by Goldman Sachs Online Savings Account: Another strong contender with competitive rates, no fees, and a user-friendly interface.

- Discover Bank Online Savings Account: Offers good rates, no fees, and 24/7 customer service. They also have a full suite of banking products.

- Capital One 360 Performance Savings: A popular choice with competitive rates, no fees, and the convenience of Capital One's broader banking ecosystem.

Product Comparison:

| Product | APY (Variable) | Fees | Key Features |

|---|---|---|---|

| Ally Bank Online Savings | ~4.25% | None | 24/7 support, buckets for goals |

| Marcus by Goldman Sachs | ~4.30% | None | No minimum deposit, strong brand |

| Discover Bank Online Savings | ~4.25% | None | Full banking suite, cash back debit |

| Capital One 360 Performance Savings | ~4.25% | None | Integrated with Capital One ecosystem |

Note: APY (Annual Percentage Yield) rates are subject to change frequently. Always check the current rates directly on the bank's website.

Automate Your Savings Set It and Forget It

The easiest way to save is to make it automatic. Set up recurring transfers from your checking account to your savings account (and investment accounts!) on payday. Even small amounts add up over time. Treat your savings like a bill you have to pay yourself first.

Investing for Young Adults Making Your Money Work Harder

Once you have an emergency fund, it's time to think about investing. This is where your money truly starts to grow and build wealth over the long term. Don't be intimidated; you don't need to be a stock market guru to start investing. The key is consistency and understanding basic principles.

Understanding Risk Tolerance and Time Horizon

As a young adult, you generally have a long time horizon (decades until retirement), which means you can afford to take on more risk. This is a huge advantage! More risk often means higher potential returns over the long run. As you get closer to retirement, you'll typically shift to lower-risk investments.

Retirement Accounts Your Best Friends

These accounts offer incredible tax advantages and are specifically designed for long-term growth. Start contributing as early as possible!

- 401(k) or 403(b): If your employer offers one, especially with a matching contribution, contribute at least enough to get the full match. That's free money! Contributions are pre-tax, reducing your taxable income now.

- Roth IRA: This is a fantastic option for young adults. You contribute after-tax money, but your withdrawals in retirement are completely tax-free. Given that your income (and thus tax bracket) is likely lower now than it will be in the future, paying taxes on contributions now can be a huge win. You can contribute up to $6,500 in 2023 (and $7,000 in 2024) if you meet income requirements.

- Traditional IRA: Contributions are often tax-deductible, and your money grows tax-deferred. You pay taxes when you withdraw in retirement.

What to Invest In Simple and Effective Options

For most young investors, simplicity and diversification are key. You don't need to pick individual stocks.

- Index Funds and ETFs: These are funds that hold a basket of stocks or bonds, designed to track a specific market index (like the S&P 500). They offer instant diversification, low fees, and generally outperform actively managed funds over the long term.

- Target-Date Funds: If you want a truly hands-off approach, a target-date fund is a great choice. You pick a fund based on your approximate retirement year (e.g., '2060 Target Date Fund'), and the fund automatically adjusts its asset allocation (more stocks when you're young, more bonds as you get older) over time.

Investment Platforms Getting Started

You'll need a brokerage account to invest. Here are some popular and highly-rated options:

- Fidelity: Offers a wide range of investment products, including their own low-cost index funds, and excellent educational resources. Great for beginners and experienced investors alike.

- Vanguard: Known for its low-cost index funds and ETFs. A favorite among passive investors. Their platform can be a bit less flashy but is highly effective.

- Charles Schwab: Another full-service brokerage with competitive fees, a wide selection of investments, and strong customer support.

- M1 Finance: A unique platform that allows you to create custom 'pies' of ETFs and stocks, then automates investing and rebalancing. Great for those who want a bit more control but still desire automation.

- Robinhood: Popular for commission-free trading of stocks and ETFs. While it has a sleek interface, be mindful of the gamification aspects and focus on long-term investing rather than speculative trading.

Product Comparison:

| Platform | Key Features | Fees | Best For |

|---|---|---|---|

| Fidelity | Broad investment selection, strong research, low-cost index funds | $0 commissions for stocks/ETFs, low expense ratios for funds | All investors, especially those seeking comprehensive tools |

| Vanguard | Industry leader in low-cost index funds and ETFs | $0 commissions for Vanguard ETFs, low expense ratios | Passive investors, long-term wealth builders |

| Charles Schwab | Full-service brokerage, good research, diverse offerings | $0 commissions for stocks/ETFs, competitive fund fees | Investors seeking a balance of tools and low costs |

| M1 Finance | Automated custom portfolios ('Pies'), rebalancing | $0 commissions, some fees for M1 Plus | Automated investing with customization, long-term focus |

| Robinhood | Commission-free trading, user-friendly app | $0 commissions, optional Gold subscription | Beginners interested in stocks/ETFs, but use with caution for long-term strategy |

Managing Debt Smartly for Young Adults Tackling Student Loans and Credit Cards

Debt can feel like a heavy burden, especially student loans and credit card debt. But with a smart strategy, you can manage it effectively and work towards becoming debt-free.

Prioritizing High-Interest Debt Credit Cards First

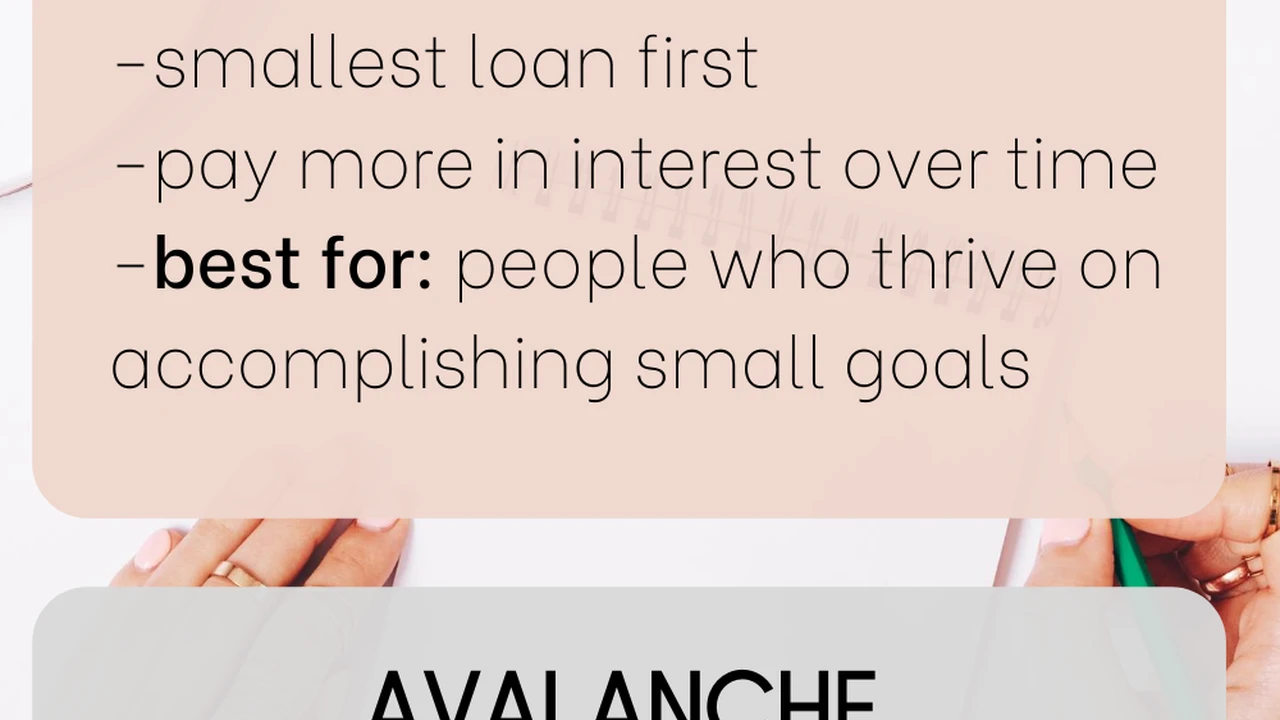

If you have credit card debt, make paying it off your top financial priority after building a small emergency fund ($1,000-$2,000). Credit card interest rates are notoriously high (often 15-25% or more), making it incredibly difficult to get ahead. Focus on paying off the card with the highest interest rate first (the 'debt avalanche' method) while making minimum payments on others.

Student Loan Strategies Income-Driven Repayment and Refinancing

Student loans are a different beast. Understand your loan types (federal vs. private) and repayment options. Federal loans offer income-driven repayment plans (IDR) that can adjust your monthly payments based on your income and family size. They also have potential for forgiveness after a certain number of payments.

For private loans, or if you have federal loans and a stable, high income, consider refinancing. Refinancing can lower your interest rate or monthly payment, but be aware that refinancing federal loans into private ones means losing federal protections like IDR and forbearance.

Avoiding Bad Debt Understanding the Difference

Not all debt is created equal. 'Good debt' might include a mortgage or student loans (if managed well) because they can lead to asset appreciation or increased earning potential. 'Bad debt' is typically high-interest consumer debt like credit cards or payday loans, which don't provide lasting value and can quickly spiral out of control. Learn to differentiate and avoid the latter.

Building Good Credit for Young Adults Your Financial Reputation

Your credit score is like your financial report card. It impacts everything from getting a loan for a car or house to renting an apartment or even getting a job. Building good credit early is essential.

How Credit Scores Are Calculated The FICO Factors

The most common credit scoring model, FICO, considers five main factors:

- Payment History (35%): Paying bills on time is the single most important factor.

- Amounts Owed (30%): How much debt you have, especially your credit utilization ratio (how much credit you're using vs. how much you have available). Keep this below 30%.

- Length of Credit History (15%): The longer your accounts have been open and in good standing, the better.

- New Credit (10%): Opening too many new accounts in a short period can be a red flag.

- Credit Mix (10%): Having a healthy mix of different types of credit (credit cards, installment loans) can be beneficial.

Starting with Your First Credit Card Responsible Use

If you're new to credit, consider a secured credit card or a student credit card. These are designed for people with limited or no credit history. A secured card requires a cash deposit, which becomes your credit limit. Use it responsibly: make small purchases you can pay off in full every month. This builds positive payment history without incurring interest.

Recommended First Credit Cards for Young Adults:

- Discover it Secured Credit Card: A popular choice for building credit. It requires a security deposit but offers cash back rewards and reports to all three major credit bureaus. After 7 months of responsible use, Discover periodically reviews your account to see if you can transition to an unsecured card and get your deposit back.

- Capital One Platinum Secured Credit Card: Another solid secured option. It offers a path to an unsecured card and reports to all three bureaus.

- Petal 2 Visa Credit Card: This card doesn't require a security deposit and uses a 'Cash Score' (based on banking history) instead of a traditional credit score for approval, making it accessible for those with no credit. It offers cash back rewards.

- Deserve EDU Mastercard for Students: Specifically designed for students (including international students), it doesn't require a Social Security Number for approval and offers cash back rewards.

Product Comparison:

| Product | Security Deposit | Rewards | Key Features | Annual Fee |

|---|---|---|---|---|

| Discover it Secured | Yes (min $200) | 1-2% cash back | Graduates to unsecured, reports to all bureaus | $0 |

| Capital One Platinum Secured | Yes (min $49, $99, or $200) | None | Path to unsecured, reports to all bureaus | $0 |

| Petal 2 Visa | No | 1-1.5% cash back | Uses 'Cash Score', no fees | $0 |

| Deserve EDU Mastercard | No | 1% cash back | For students (incl. international), no SSN required | $0 |

Monitoring Your Credit Regularly Free Credit Reports

You're entitled to a free credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months via AnnualCreditReport.com. Check them for errors, which can negatively impact your score. Many credit card companies and banks also offer free credit score monitoring services (like Credit Karma or Experian Boost) that can help you keep an eye on your score and report.

Protecting Your Finances for Young Adults Guarding Against Identity Theft and Scams

As you become more financially independent, you also become a target for scammers and identity thieves. Protecting your personal and financial information is paramount.

Understanding Common Scams Phishing and Impersonation

Be wary of unsolicited emails, texts, or calls asking for personal information (Social Security number, bank account details, passwords). Government agencies, banks, and reputable companies rarely ask for this sensitive information via these channels. Always verify the sender or caller independently.

Strong Passwords and Two-Factor Authentication Your Digital Fortress

Use unique, strong passwords for all your financial accounts. Consider a password manager to keep track of them. Enable two-factor authentication (2FA) wherever possible. This adds an extra layer of security, usually requiring a code from your phone in addition to your password.

Freezing Your Credit The Ultimate Protection

If you're not actively applying for new credit, consider freezing your credit with all three major credit bureaus. This prevents anyone, including identity thieves, from opening new accounts in your name. You can temporarily unfreeze it when you need to apply for credit. It's free and highly effective.

Financial Education Continues Lifelong Learning for Financial Freedom

This guide is just the beginning! Financial planning is an ongoing journey. The world of finance is constantly evolving, and your personal circumstances will change. Make it a habit to continue learning about personal finance. Read books, follow reputable financial blogs, listen to podcasts, and stay informed. The more you know, the better equipped you'll be to make smart decisions and adapt to whatever life throws your way.

Remember, financial planning isn't about perfection; it's about progress. Start small, stay consistent, and celebrate your wins along the way. Your future self will absolutely thank you for taking these steps today. You've got this!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)