FICO vs VantageScore Key Differences Explained

Understand the core differences between FICO and VantageScore credit models and how they impact your creditworthiness.

Understand the core differences between FICO and VantageScore credit models and how they impact your creditworthiness.

FICO vs VantageScore Key Differences Explained

Understanding Credit Scoring Models The Foundation of Your Financial Life

Hey there, ever wondered why your credit score seems to pop up everywhere, from applying for a new apartment to getting a car loan? It's because your credit score is a super important number that lenders use to figure out how risky it might be to lend you money. Think of it as your financial report card. But here's a little secret: there isn't just one credit score. In fact, there are hundreds! The two big players you'll hear about most often are FICO and VantageScore. While both aim to do the same thing – predict your likelihood of repaying debt – they go about it in slightly different ways, and understanding these differences can be a game-changer for your financial health, especially if you're navigating the US or Southeast Asian markets where credit systems are evolving. So, what exactly are FICO and VantageScore, and why should you care about their distinctions? Let's dive deep into the nitty-gritty, comparing their methodologies, what factors they prioritize, and how these nuances can affect your financial opportunities. We'll also look at some specific products and scenarios where one might be more prevalent than the other, giving you the insider knowledge to optimize your credit profile.FICO Score Deep Dive The Industry Standard for Decades

FICO, short for Fair Isaac Corporation, has been around since 1956 and is pretty much the granddaddy of credit scoring. For a long time, it was the only game in town, and even today, it's estimated that over 90% of top lenders use FICO scores in their decision-making process. This means if you're applying for a mortgage, a car loan, or even some credit cards, there's a very high chance the lender is pulling a FICO score.FICO's Secret Sauce What Factors Matter Most

FICO scores are calculated based on information from your credit reports, which are compiled by the three major credit bureaus: Experian, Equifax, and TransUnion. While the exact algorithms are proprietary (meaning they keep them secret!), FICO openly shares the general categories and their approximate weighting:- Payment History (35%): This is the biggest piece of the pie. Paying your bills on time, every time, is crucial. Late payments, bankruptcies, foreclosures, and collections accounts can severely ding your score.

- Amounts Owed (30%): This isn't just about how much debt you have, but also your credit utilization ratio – how much credit you're using compared to your total available credit. Keeping this ratio low (ideally below 30%) is key.

- Length of Credit History (15%): The longer your credit accounts have been open and in good standing, the better. This shows lenders you have a proven track record.

- New Credit (10%): Opening too many new credit accounts in a short period can be seen as risky. Each hard inquiry (when a lender checks your credit for a new application) can temporarily lower your score.

- Credit Mix (10%): Having a healthy mix of different types of credit (like credit cards, installment loans, and mortgages) can positively impact your score, showing you can manage various forms of debt responsibly.

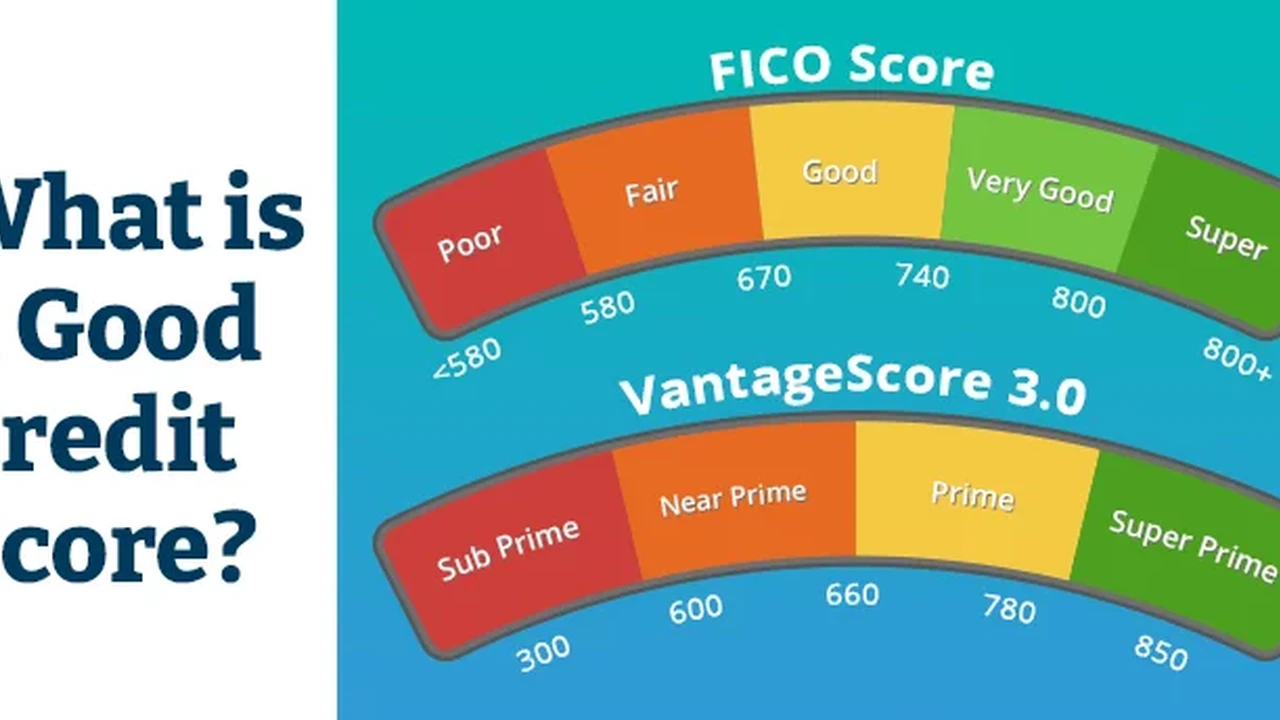

FICO Score Ranges and What They Mean for You

FICO scores typically range from 300 to 850. Here's a general breakdown:- 800-850: Exceptional. You're a credit superstar! You'll get the best rates and terms.

- 740-799: Very Good. Still excellent, you'll qualify for most loans with favorable terms.

- 670-739: Good. This is considered average to good. You'll likely qualify for most credit products, though not always with the absolute best rates.

- 580-669: Fair. You might face higher interest rates or have fewer options. This is where credit repair often becomes a focus.

- 300-579: Poor. Lenders will see you as a high risk. Getting approved for new credit will be challenging, and interest rates will be very high.

FICO Versions and Their Specific Applications

It's important to note that there isn't just one FICO score. FICO has developed numerous versions over the years, tailored for different types of lending and industries. For example:- FICO Score 8: This is the most widely used version. It's a general-purpose score that many lenders use for credit cards and personal loans.

- FICO Score 9: A newer version that gives less weight to paid collection accounts and medical collections.

- FICO Auto Scores (e.g., FICO Auto Score 8, 9): These are specifically designed for auto lenders and place more emphasis on your history with car loans.

- FICO Bankcard Scores (e.g., FICO Bankcard Score 8, 9): Used by credit card issuers, these scores focus on your credit card usage and payment patterns.

- FICO Mortgage Scores (e.g., FICO Score 2, 4, 5): Mortgage lenders often use older FICO versions (sometimes called 'classic' FICO scores) because they have a long history of predicting mortgage default risk. This is a crucial point for anyone looking to buy a home.

VantageScore Explained The Modern Alternative

VantageScore is a newer credit scoring model, introduced in 2006 as a joint venture by the three major credit bureaus (Experian, Equifax, and TransUnion). Their goal was to create a more consistent and consumer-friendly scoring model that could compete with FICO. While not as widely adopted as FICO, VantageScore is gaining traction, especially with free credit monitoring services and some lenders.VantageScore's Scoring Factors How They Differ

VantageScore also uses information from your credit reports, but its weighting and terminology are slightly different. They categorize their factors as follows:- Total Credit Usage, Balance, and Available Credit (Extremely Influential): Similar to FICO's 'Amounts Owed,' this looks at your credit utilization and overall debt levels.

- Credit Mix and Experience (Highly Influential): This combines the length of your credit history and the types of credit you manage.

- Payment History (Moderately Influential): While still very important, VantageScore gives it slightly less weight than FICO.

- New Credit (Less Influential): The impact of recent credit applications is less pronounced than with FICO.

- Age of Credit History (Less Influential): The length of time your accounts have been open.

VantageScore Ranges and Their Implications

VantageScore also uses a 300-850 range, but their categories are slightly different:- 781-850: Excellent. Top-tier creditworthiness.

- 661-780: Good. Solid credit, good access to credit products.

- 601-660: Fair. You might qualify for some credit, but with higher rates.

- 500-600: Poor. Limited credit options, high interest rates.

- 300-499: Very Poor. Very challenging to get approved for new credit.

Key Differences Between FICO and VantageScore Credit Models

Now that we've looked at each individually, let's put them side-by-side to highlight the most important distinctions:Minimum Credit History Requirements for Scoring

As mentioned, this is a big one. FICO generally needs at least six months of credit history and activity. VantageScore can score you with just one month of history. This makes VantageScore particularly useful for:- Young adults: Just starting out with their first credit card.

- Immigrants: New to the US or Southeast Asian credit systems.

- Credit re-builders: Those who have had a long period without active credit.

Impact of Paid Collections and Medical Debt

This is another significant divergence. Older FICO versions (like FICO Score 8) still consider paid collection accounts as negative marks. However, FICO Score 9 and all VantageScore models give less weight to paid collection accounts and often ignore medical collections entirely. This is a huge win for consumers who have struggled with medical debt or have worked hard to pay off old collections.Treatment of Hard Inquiries

Both models consider hard inquiries (when you apply for new credit) as a negative factor, but VantageScore tends to be a bit more forgiving. It also has a 'softening' period where multiple inquiries for the same type of loan (like a mortgage or auto loan) within a short window (typically 14-45 days, depending on the model) are treated as a single inquiry. FICO also has this 'rate shopping' logic, but the window can vary.Weighting of Credit Factors

While both models look at similar categories, their emphasis differs. FICO places a slightly heavier emphasis on payment history and amounts owed. VantageScore gives more weight to overall credit usage and balance, and credit mix/experience. These subtle differences can lead to variations in your score depending on your specific credit profile.Prevalence in Lending Decisions

FICO remains the dominant force in traditional lending, especially for mortgages, auto loans, and many credit cards. VantageScore is more commonly used by free credit monitoring services (like Credit Karma, which uses VantageScore 3.0) and some smaller lenders or for tenant screening. It's also gaining traction in the personal loan space.Where to Check Your FICO and VantageScore Scores and Why It Matters

Knowing where to find your scores is just as important as understanding them. You'll likely encounter both, and it's good to monitor both, even if one is more critical for your immediate goals.Accessing Your FICO Scores Specific Products and Services

Since FICO is proprietary, you usually have to pay for direct access to your FICO scores, or get them through a service that partners with FICO. Here are some common ways:- MyFICO.com: This is the official source. They offer various plans, from monthly subscriptions to one-time reports. A basic plan might cost around $19.95/month for one bureau's FICO Score 8, while a more comprehensive plan covering all three bureaus and multiple FICO versions could be $39.95/month or more. This is the most detailed way to see the exact FICO scores lenders use.

- Credit Card Issuers: Many credit card companies now offer free FICO scores to their cardholders. Examples include:

- Discover: Provides FICO Score 8 based on TransUnion data.

- Bank of America: Offers FICO Score 8 based on TransUnion data.

- Citi: Provides FICO Score 8 based on Equifax data.

- Wells Fargo: Offers FICO Score 9 based on Experian data.

- American Express: Provides FICO Score 8 based on Experian data.

- Experian.com: Experian offers a free FICO Score 8 (based on Experian data) if you sign up for their free credit monitoring service. They also have paid plans for more detailed FICO scores.

- Other Financial Institutions: Some banks and credit unions also provide free FICO scores to their customers. Check with your primary bank.

Accessing Your VantageScore Scores Popular Free Platforms

VantageScore is much more accessible for free, making it a great tool for general credit monitoring.- Credit Karma: This is probably the most well-known platform for free VantageScore access. They provide VantageScore 3.0 from TransUnion and Equifax. While not FICO, it's excellent for tracking trends and identifying changes in your credit report.

- Credit Sesame: Similar to Credit Karma, Credit Sesame offers a free VantageScore 3.0 based on TransUnion data.

- NerdWallet: Provides a free VantageScore 3.0 from TransUnion.

- Many Banks and Credit Unions: A growing number of financial institutions offer free VantageScore access to their customers.

- AnnualCreditReport.com: While this site primarily gives you free credit reports (which you should check annually!), some services linked from there might offer a free VantageScore.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)