Understanding the Fair Debt Collection Practices Act

Familiarize yourself with the FDCPA to understand your rights and protections against unfair debt collection practices.

Familiarize yourself with the FDCPA to understand your rights and protections against unfair debt collection practices.

Understanding the Fair Debt Collection Practices Act

What is the Fair Debt Collection Practices Act FDCPA Explained

Hey there! Ever felt like you're being hounded by debt collectors and wondered if there are any rules they have to follow? Well, you're in luck, because there absolutely are! The Fair Debt Collection Practices Act, or FDCPA for short, is a federal law in the United States that puts some pretty strict boundaries on what third-party debt collectors can and cannot do when they're trying to collect a debt from you. Think of it as your shield against harassment, deception, and unfair practices. This law was enacted way back in 1977 because, let's face it, some debt collectors were getting a little too aggressive and unethical. It's all about protecting consumers like you from abusive debt collection tactics.

Now, it's super important to understand who the FDCPA actually covers. Generally, it applies to third-party debt collectors, which means companies or individuals who collect debts on behalf of someone else. So, if you owe money directly to a credit card company, a bank, or a hospital, and they're trying to collect it themselves, the FDCPA usually doesn't apply to them. However, if they hire a collection agency, or sell your debt to a debt buyer, then those entities are covered. Also, if a creditor uses a different name to collect its own debts, or if they originated the debt and then transferred it to another entity they control, they might also fall under the FDCPA's umbrella. It can get a bit nuanced, but the main takeaway is that it's designed to regulate those professional debt collectors who are often the most persistent.

Your Rights Under the FDCPA Knowing Your Protections

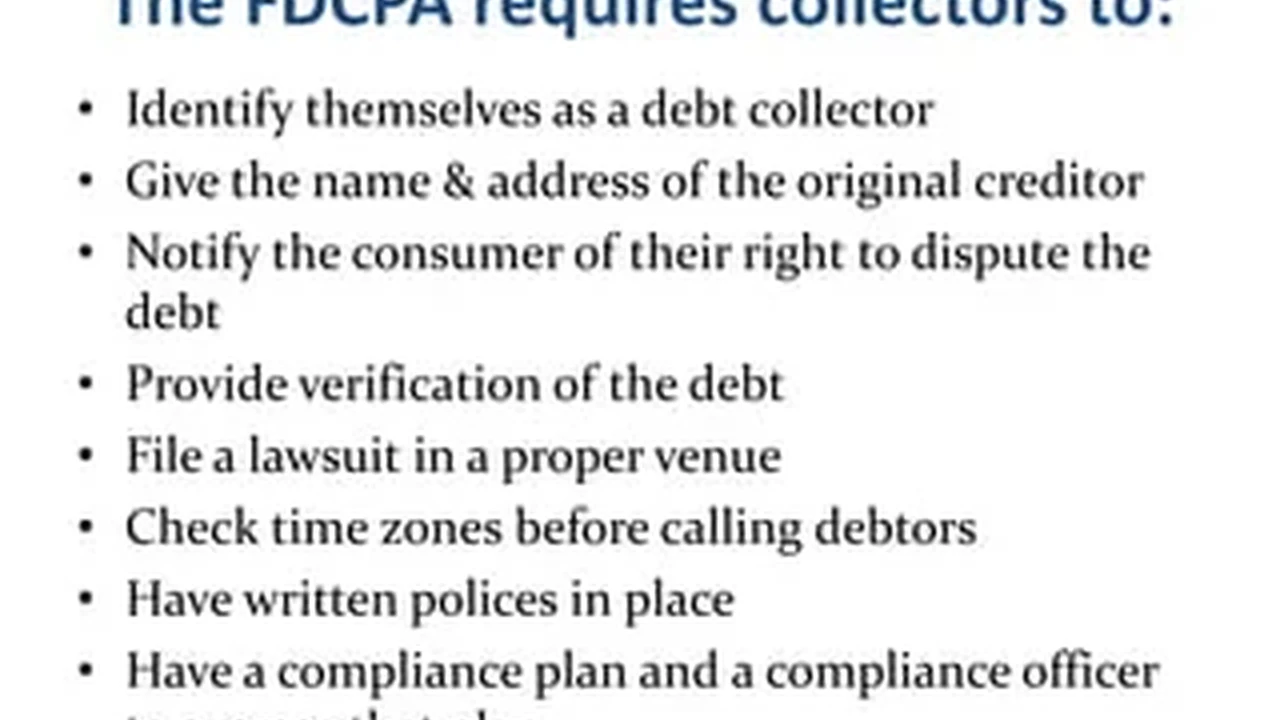

Alright, so you know the FDCPA exists, but what exactly does it do for you? A whole lot, actually! This law gives you a bunch of rights that can really level the playing field when you're dealing with debt collectors. Let's break down some of the most important ones:

Right to Debt Validation Requesting Proof of Debt

This is a big one! When a debt collector first contacts you, or within five days of their initial contact, they have to send you a written notice. This notice needs to include the amount of the debt, the name of the creditor you owe, and a statement that you have 30 days to dispute the debt. If you dispute the debt in writing within that 30-day window, the collector has to stop all collection efforts until they send you verification of the debt. This verification should include things like copies of the original contract, payment history, and anything else that proves you actually owe the money. It's your right to ask for proof, and they have to provide it before they can continue trying to collect.

Prohibited Debt Collector Practices What They Cannot Do

The FDCPA is very clear about what debt collectors absolutely cannot do. This is where your protection really kicks in. They cannot:

- Harass you: This means no repeated phone calls designed to annoy or abuse you, no threats of violence, and no obscene or profane language.

- Make false statements: They can't lie about the amount you owe, pretend to be lawyers or government officials, or falsely claim that you'll be arrested if you don't pay.

- Threaten legal action they can't or won't take: They can't say they'll sue you if they have no intention of doing so, or if they're legally unable to.

- Use unfair practices: This includes things like trying to collect interest or fees that aren't allowed by law or your original agreement, or depositing a post-dated check prematurely.

- Contact you at inconvenient times or places: Generally, they can't call you before 8:00 AM or after 9:00 PM in your time zone, unless you agree to it. They also can't call you at work if they know your employer prohibits such calls.

- Discuss your debt with third parties: They can't tell your friends, family, or employer about your debt, except for very limited circumstances like finding out your location.

- Threaten to seize your property: Unless they have a court order, they can't threaten to take your car, house, or other belongings.

Stopping Debt Collector Communication Your Right to Cease and Desist

Feeling overwhelmed by calls and letters? You have the power to make them stop! You can send a written letter to the debt collector telling them to cease all communication. Once they receive this letter, they can only contact you one more time to tell you they're stopping contact or to inform you of a specific action they might take (like filing a lawsuit). It's a powerful tool to regain some peace of mind, but remember, it doesn't make the debt go away. You still owe the money, and they could still pursue legal action, but at least the constant calls will stop.

Identifying FDCPA Violations Recognizing Unfair Practices

Knowing your rights is one thing, but recognizing when those rights are being violated is key. Debt collectors can be sneaky, so it's important to be vigilant. Here are some common red flags that might indicate an FDCPA violation:

- Excessive or repetitive calls: If they're calling you multiple times a day, every day, especially if you've asked them to stop, that's a problem.

- Calls to your workplace after you've told them not to: If you've informed them that your employer doesn't allow personal calls, and they keep calling, that's a violation.

- Threats of arrest or imprisonment: This is a huge no-no. Debt is a civil matter, not a criminal one, so they can't have you arrested for not paying.

- Threats of violence or harm: Any threat of physical harm is absolutely illegal and should be reported immediately.

- Sharing your debt information with others: If your neighbor, coworker, or family member tells you the debt collector called them about your debt, that's a violation.

- Refusal to validate the debt: If you send a written request for validation within 30 days and they continue collection efforts without providing it, they're breaking the law.

- Using abusive or profane language: There's no excuse for a debt collector to use offensive language.

- Calling at odd hours: If they're calling you at 6 AM or 11 PM, that's generally a violation.

- Demanding payment for a debt you don't recognize or believe you owe: Always validate!

Steps to Take When Your FDCPA Rights Are Violated Protecting Yourself

So, you suspect a debt collector has violated your FDCPA rights. Don't just sit there and take it! You have options. Here's what you should do:

Document Everything Keeping Detailed Records

This is probably the most important step. Keep a meticulous record of every interaction you have with the debt collector. This includes:

- Dates and times of calls: Note down when they called and how long the call lasted.

- Names of the collectors: Ask for their name and the name of their company.

- What was said: Briefly summarize the conversation, especially any threats, abusive language, or false statements.

- Copies of all correspondence: Keep every letter they send you and make copies of any letters you send them (especially your debt validation request and cease and desist letter). Send your letters via certified mail with a return receipt requested so you have proof they received it.

- Voicemails: If they leave voicemails, save them.

Filing a Complaint Reporting FDCPA Violations

Once you have your documentation, you can file a complaint with the appropriate authorities. This is how you get the ball rolling and hold these collectors accountable. Here are the main places to report:

- Consumer Financial Protection Bureau (CFPB): This is a federal agency dedicated to protecting consumers in the financial marketplace. They have an easy-to-use online complaint system. They can investigate your complaint and take action against the debt collector.

- Federal Trade Commission (FTC): The FTC also handles complaints about unfair and deceptive business practices, including those by debt collectors.

- Your State Attorney General's Office: Many states have their own laws regarding debt collection, and your state's Attorney General can often help.

Seeking Legal Counsel When to Contact an Attorney

If the violations are severe, persistent, or if you're feeling overwhelmed, it might be time to talk to an attorney. Many consumer protection lawyers specialize in FDCPA cases and offer free consultations. If a debt collector has violated the FDCPA, you might be able to sue them for damages, including actual damages (like lost wages due to stress) and statutory damages (up to $1,000). The FDCPA also allows for the recovery of attorney's fees, which means you might not have to pay anything out of pocket if you win your case. An attorney can help you understand your rights, evaluate your case, and guide you through the legal process.

Practical Tools and Resources for Debt Collection Issues Supporting Your Fight

Navigating debt collection can be tough, but there are tools and resources out there to help you. Here are a few that can make a real difference:

Recommended Apps for Call Recording and Documentation

While some states require two-party consent for call recording, if you're in a one-party consent state (or if you inform the collector you're recording), these apps can be invaluable for documenting conversations:

- Truecaller: This app is great for identifying unknown callers, blocking spam calls, and in some regions, it offers call recording features. It's widely available on both Android and iOS.

- ACR Call Recorder (Android): A popular choice for Android users, ACR allows you to record incoming and outgoing calls automatically or manually. It offers various cloud storage integrations.

- TapeACall Pro (iOS/Android): This app is a subscription-based service that offers reliable call recording for both platforms. It's often used by professionals for its ease of use and quality.

Important Note on Call Recording: Always be aware of your local and state laws regarding call recording. In some states, it's illegal to record a conversation without the consent of all parties involved. If you're unsure, it's best to err on the side of caution or consult with a legal professional.

Online Resources for FDCPA Information and Templates

The internet is a treasure trove of information. Here are some reliable sources:

- Consumer Financial Protection Bureau (CFPB) Website: The CFPB's website (consumerfinance.gov) is an official and comprehensive source for FDCPA information, including sample letters for disputing debts and stopping communication. They also have a portal for filing complaints.

- Federal Trade Commission (FTC) Website: The FTC (ftc.gov) also provides excellent consumer information on debt collection, scams, and your rights.

- National Consumer Law Center (NCLC): While primarily for legal professionals, the NCLC website (nclc.org) offers valuable insights and publications on consumer law, including debt collection.

- Legal Aid Organizations: Many local legal aid societies offer free or low-cost legal assistance to individuals who can't afford an attorney. A quick search for 'legal aid [your city/state]' can help you find one.

Comparison of Legal Services for FDCPA Cases

If you decide to pursue legal action, here's a general comparison of options:

- Private Consumer Protection Attorneys: These lawyers specialize in consumer rights and often work on a contingency basis for FDCPA cases, meaning they only get paid if you win. They have extensive experience and can navigate complex legal procedures.

- Legal Aid Societies: As mentioned, these organizations provide free or low-cost legal services. Their availability depends on your income and the severity of your case. They are a great option if you qualify.

- Online Legal Services (e.g., LegalZoom, Rocket Lawyer): While useful for drafting basic legal documents, these services are generally not suitable for representing you in a lawsuit against a debt collector. They can help with creating cease and desist letters, but for actual litigation, a dedicated attorney is usually necessary.

Pricing for Legal Services: For FDCPA cases, many private attorneys offer free initial consultations. If they take your case, it's often on a contingency fee basis, meaning their fees are a percentage of the settlement or award you receive. This is because the FDCPA allows for the recovery of attorney's fees from the violating debt collector. So, if you have a strong case, you might not pay anything upfront. For legal aid, services are typically free or based on a sliding scale depending on your income.

Common FDCPA Misconceptions Separating Fact from Fiction

There's a lot of misinformation out there about debt collection. Let's clear up some common myths:

- Myth: The FDCPA applies to all debt collectors. Fact: It primarily applies to third-party debt collectors. Original creditors collecting their own debts are generally not covered, though some states have laws that cover them.

- Myth: Sending a cease and desist letter makes the debt disappear. Fact: It stops communication, but the debt is still owed. The collector can still pursue legal action.

- Myth: You can be arrested for not paying a civil debt. Fact: This is absolutely false. Debt is a civil matter, and you cannot be arrested or jailed for failing to pay a consumer debt.

- Myth: Debt collectors can call anyone about your debt. Fact: They can only contact third parties (like employers or relatives) to find out your location, and they can't reveal that they're a debt collector or that you owe money.

- Myth: You have to pay a debt if a collector says you do. Fact: Always validate the debt first! Don't pay anything until you've confirmed it's legitimate and yours.

State Specific Debt Collection Laws How They Complement FDCPA

While the FDCPA is a federal law, many states have their own debt collection laws that offer additional protections. These state laws can sometimes be even stronger than the FDCPA, covering original creditors or providing more stringent rules on communication and practices. For example, some states might have shorter statutes of limitations for debt collection or stricter rules on what constitutes harassment. It's always a good idea to research your specific state's laws or consult with a local attorney to understand the full scope of your protections. These state laws work in conjunction with the FDCPA, giving you an extra layer of defense against unfair collection tactics.

Empowering Yourself Taking Control of Your Debt Situation

Dealing with debt collectors can be incredibly stressful, but remember, you're not powerless. The FDCPA is a powerful tool designed to protect you. By understanding your rights, documenting everything, and knowing when to seek help, you can effectively navigate the world of debt collection and ensure you're treated fairly. Don't let fear or intimidation prevent you from asserting your rights. Take control, educate yourself, and stand up for what's right. You've got this!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)