Understanding Compound Interest Your Wealth Builder

A comprehensive guide to financial planning for young adults covering budgeting, saving, and investing.

A comprehensive guide to financial planning for young adults covering budgeting, saving, and investing.

Financial Planning for Young Adults Essential Guide

Why Financial Planning Matters for Young Adults Your Future Starts Now

Hey there, young adult! Ever feel like everyone around you is talking about money, but no one actually teaches you how to manage it? You're not alone. Financial planning might sound like something your parents or grandparents do, but trust me, getting a handle on your finances early on is one of the smartest moves you can make. It's not just about saving for a rainy day; it's about building a solid foundation for your future, whether that's buying a house, traveling the world, starting a business, or simply having peace of mind. This guide is designed to cut through the jargon and give you actionable steps to take control of your money, starting today. We'll cover everything from setting up a budget that actually works to smart saving strategies and even dipping your toes into the world of investing. Think of this as your personal roadmap to financial freedom.

Budgeting Basics for Young Adults Creating Your First Financial Blueprint

Budgeting. The word itself can sound restrictive, but it's actually your key to financial freedom. A budget isn't about telling you what you can't spend; it's about showing you where your money is going and helping you allocate it to what truly matters to you. For young adults, this is especially crucial as you navigate new expenses like rent, student loan payments, and maybe even your first 'adult' bills. Let's break down how to create a budget that's realistic and sustainable.

Tracking Your Income and Expenses Understanding Your Cash Flow

The first step in any budget is knowing your numbers. How much money is coming in, and how much is going out? This might seem obvious, but many people are surprised when they actually track their spending. For income, include your net pay (after taxes), any freelance earnings, or other regular sources of money. For expenses, this is where it gets interesting. Categorize everything: rent, utilities, groceries, transportation, student loan payments, subscriptions (Netflix, Spotify, gym memberships), dining out, entertainment, clothes, and even those daily coffees. Don't forget irregular expenses like car maintenance or annual subscriptions. You can use a simple spreadsheet, a notebook, or one of the many budgeting apps we'll discuss later.

Setting Financial Goals for Young Adults What Do You Want Your Money to Do

Before you start cutting expenses, think about what you're saving for. Do you want to pay off student loans faster? Save for a down payment on a car or house? Build an emergency fund? Travel? Having clear, specific goals will motivate you and give purpose to your budgeting efforts. Make your goals SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, instead of 'save money,' try 'save $5,000 for a down payment on a car in 12 months.'

Choosing a Budgeting Method That Fits Your Lifestyle The 50/30/20 Rule and Beyond

There isn't a one-size-fits-all budgeting method. Here are a few popular ones that work well for young adults:

- The 50/30/20 Rule: This is a great starting point. Allocate 50% of your after-tax income to needs (rent, utilities, groceries, transportation, minimum loan payments), 30% to wants (dining out, entertainment, hobbies, shopping), and 20% to savings and debt repayment (emergency fund, investments, extra loan payments). It's simple and flexible.

- Zero-Based Budgeting: Every dollar has a job. You assign every dollar of your income to a specific category until your income minus your expenses equals zero. This method requires more tracking but gives you complete control.

- Envelope System: For those who prefer cash. Allocate a certain amount of cash to different spending categories (e.g., groceries, entertainment) and put it in physical envelopes. Once an envelope is empty, you stop spending in that category until the next pay period.

- Pay Yourself First: This isn't a full budgeting system but a powerful principle. As soon as you get paid, immediately transfer a set amount to your savings or investment accounts. What's left is what you have to spend. This ensures your savings goals are prioritized.

Saving Strategies for Young Adults Building Your Financial Safety Net and Future Wealth

Once you have a budget, the next step is to make your money work for you through smart saving. This isn't just about putting money aside; it's about strategically allocating funds for different purposes.

Building an Emergency Fund Your Financial Buffer

This is non-negotiable. An emergency fund is a stash of money specifically for unexpected expenses like job loss, medical emergencies, or car repairs. Aim for at least 3-6 months' worth of essential living expenses. Keep this money in a separate, easily accessible, high-yield savings account, not your checking account, and definitely not invested in the stock market where it could lose value quickly.

High Yield Savings Accounts Maximizing Your Savings Growth

Don't let your emergency fund or short-term savings sit in a traditional savings account earning next to nothing. High-yield savings accounts (HYSAs) offer significantly better interest rates, allowing your money to grow faster. They are typically offered by online banks, which have lower overheads and can pass those savings on to you in the form of higher interest rates. They are FDIC-insured, so your money is safe.

Recommended High Yield Savings Accounts for Young Adults

- Ally Bank Online Savings Account:

- Features: Competitive APY, no monthly maintenance fees, no minimum balance requirements, 24/7 customer service, easy online transfers.

- Use Case: Excellent for emergency funds, short-term savings goals (e.g., vacation, new gadget), and general savings.

- Comparison: Often cited for its user-friendly interface and consistent high rates.

- Pricing: Free to open and maintain.

- Marcus by Goldman Sachs Online Savings Account:

- Features: Strong APY, no fees, no minimum deposit to open, excellent customer service, option for linked external accounts.

- Use Case: Ideal for those who want a reliable online bank with competitive rates and a trusted name.

- Comparison: Similar to Ally in terms of features and rates, often a close competitor.

- Pricing: Free to open and maintain.

- Discover Bank Online Savings Account:

- Features: Competitive APY, no monthly fees, no minimum balance, 24/7 U.S.-based customer service, and often integrates well if you already have Discover credit cards.

- Use Case: Good for those who value integrated banking services and strong customer support.

- Comparison: Offers a solid all-around package, sometimes with slightly lower rates than pure online competitors but with added convenience for existing Discover customers.

- Pricing: Free to open and maintain.

Automating Your Savings Making It Effortless

The easiest way to save is to make it automatic. Set up automatic transfers from your checking account to your savings and investment accounts on payday. Treat these transfers like any other bill. If you don't see the money, you're less likely to spend it. Even small, consistent transfers add up significantly over time thanks to the magic of compound interest.

Saving for Short Term vs Long Term Goals Different Buckets for Different Dreams

It's helpful to have different 'buckets' for your savings. Your emergency fund is one bucket. Another might be for short-term goals (e.g., a new laptop, a concert ticket, a weekend trip). These can stay in your HYSA. For long-term goals (retirement, a house down payment years away), you'll want to consider investing, which we'll get to next.

Investing for Young Adults Growing Your Wealth Over Time

Investing might sound intimidating, but it's one of the most powerful tools for building long-term wealth. The earlier you start, the more time your money has to grow through compound interest. You don't need to be rich to start investing; even small amounts can make a big difference over decades.

Understanding Investment Basics Risk and Return for Beginners

Every investment carries some level of risk, but generally, higher potential returns come with higher risk. For young adults with a long time horizon (decades until retirement), you can afford to take on more risk because you have time to recover from market downturns. Common investment vehicles include:

- Stocks: Represent ownership in a company. Can offer high returns but are volatile.

- Bonds: Loans to governments or corporations. Generally less risky than stocks but offer lower returns.

- Mutual Funds and ETFs (Exchange-Traded Funds): Collections of stocks, bonds, or other assets. They offer diversification, meaning you're not putting all your eggs in one basket. This is often the best starting point for beginners.

Retirement Accounts for Young Adults Maximize Your Tax Advantages

These are your best friends for long-term wealth building due to their tax benefits:

- 401(k) or 403(b): If your employer offers one, contribute at least enough to get the full employer match – it's free money! Contributions are pre-tax, reducing your taxable income now, and grow tax-deferred until retirement.

- Roth IRA: Contributions are made with after-tax dollars, but your withdrawals in retirement are completely tax-free. This is often ideal for young adults who expect to be in a higher tax bracket later in their careers. You can contribute up to a certain limit each year.

- Traditional IRA: Contributions may be tax-deductible, and your money grows tax-deferred. You pay taxes when you withdraw in retirement.

Robo-Advisors and Brokerage Accounts Easy Investing for Beginners

For young adults just starting, robo-advisors are a fantastic option. They use algorithms to manage your investments based on your financial goals and risk tolerance, often with very low fees. If you prefer more control or want to pick individual stocks, a traditional brokerage account is the way to go.

Recommended Investment Platforms for Young Adults

- Fidelity Go (Robo-Advisor):

- Features: Automated investing with low fees, no advisory fees for balances under $25,000, diversified portfolios, access to Fidelity's extensive research and customer support.

- Use Case: Excellent for beginners who want a hands-off approach to investing, especially for long-term goals like retirement or general wealth building.

- Comparison: Competes with other robo-advisors like Betterment and Wealthfront but offers the backing of a major financial institution.

- Pricing: No advisory fee for balances under $25,000; 0.35% annual advisory fee for balances over $25,000.

- Vanguard (DIY Brokerage):

- Features: Known for low-cost index funds and ETFs, strong long-term performance, investor-owned structure means lower fees, wide range of investment options.

- Use Case: Ideal for young adults who want to take a more active role in choosing their investments, particularly those interested in passive investing through index funds.

- Comparison: A leader in low-cost investing, often preferred by those who want to avoid active management fees.

- Pricing: No commissions for online stock and ETF trades; expense ratios for funds are among the lowest in the industry.

- Charles Schwab (Hybrid Robo-Advisor and Brokerage):

- Features: Offers both Schwab Intelligent Portfolios (robo-advisor with no advisory fees) and a full-service brokerage, extensive research tools, excellent customer service, physical branches available.

- Use Case: Great for young adults who want flexibility – start with a robo-advisor and transition to self-directed investing as they gain confidence, or use both.

- Comparison: Provides a comprehensive suite of services, blending automated convenience with traditional brokerage options.

- Pricing: Schwab Intelligent Portfolios have no advisory fees (though underlying ETFs have expense ratios); no commissions for online stock and ETF trades.

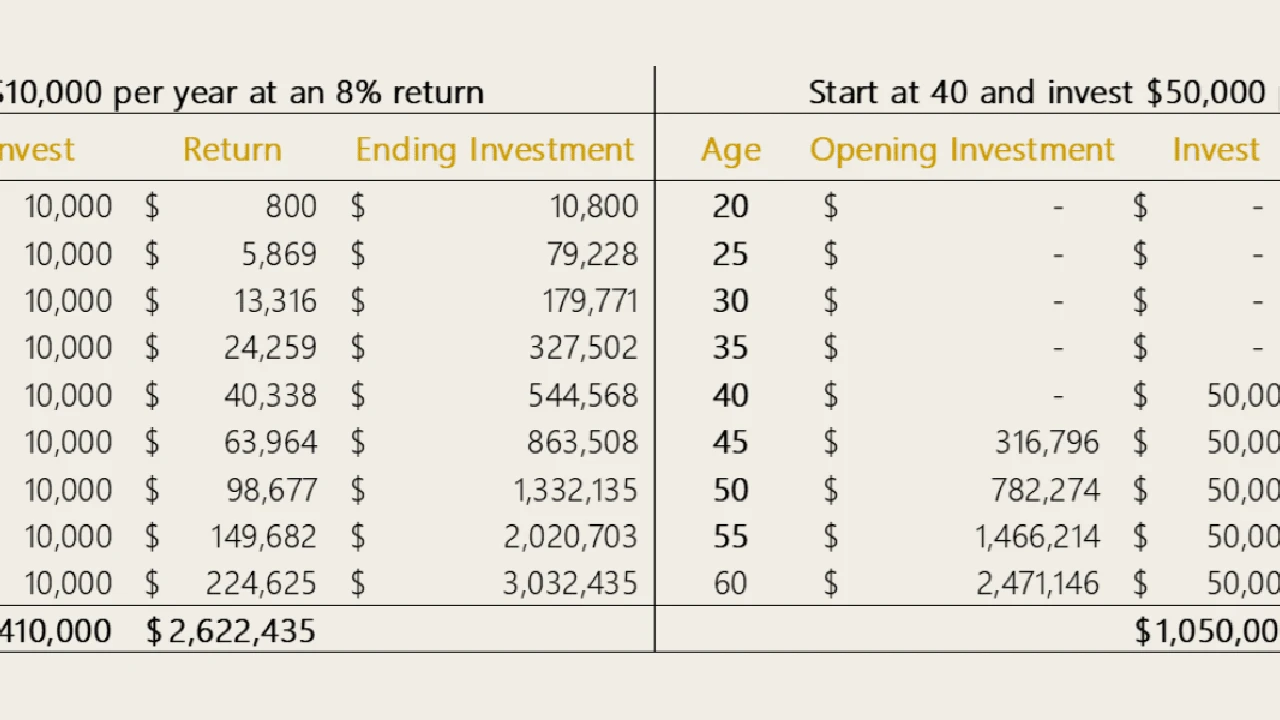

The Power of Compound Interest Start Early, Invest Consistently

This is the 'eighth wonder of the world,' as Einstein supposedly called it. Compound interest means your earnings also earn interest. The longer your money is invested, the more time it has to compound and grow exponentially. Even small, consistent contributions over decades can turn into substantial wealth. Don't underestimate the power of starting early!

Managing Debt as a Young Adult Strategies for Student Loans and Credit Cards

Debt is a reality for many young adults, especially student loans and credit card balances. The key is to manage it strategically and pay it down efficiently to free up your finances for other goals.

Student Loan Repayment Strategies Income Driven Plans and Refinancing

Student loans can feel overwhelming, but you have options. Understand your loan types (federal vs. private) and repayment plans. Federal loans offer income-driven repayment (IDR) plans that adjust your monthly payment based on your income and family size. They also offer potential for loan forgiveness after a certain number of payments. For private loans, or if you have high-interest federal loans and a stable job, consider refinancing to a lower interest rate, but be aware you might lose federal loan protections.

Credit Card Debt Avoidance and Payoff Tactics

Credit cards can be a useful tool for building credit, but they can also be a trap if not managed carefully. Always try to pay your statement balance in full each month to avoid interest charges. If you carry a balance, prioritize paying off the card with the highest interest rate first (the 'debt avalanche' method) or the smallest balance first for psychological wins (the 'debt snowball' method). Avoid opening too many cards, and be mindful of your credit utilization ratio (how much credit you're using compared to your total available credit).

Building Good Credit Habits for Your Future Financial Health

Your credit score is like your financial report card. A good score opens doors to lower interest rates on loans, easier apartment rentals, and even better insurance premiums. To build good credit:

- Pay all your bills on time, every time.

- Keep your credit utilization low (ideally below 30%).

- Don't close old credit accounts, as this can shorten your credit history.

- Regularly check your credit report for errors (you can get a free report annually from AnnualCreditReport.com).

Protecting Your Finances Essential Insurance and Identity Theft Prevention

Financial planning isn't just about growing your money; it's also about protecting it from unexpected events. For young adults, this means understanding basic insurance and safeguarding your personal information.

Understanding Basic Insurance Needs Health Auto Renters

- Health Insurance: Crucial for covering medical expenses. If you're under 26, you might still be on your parents' plan. Otherwise, explore options through your employer, the Affordable Care Act marketplace, or private plans.

- Auto Insurance: A legal requirement in most places if you own a car. Shop around for the best rates and coverage.

- Renters Insurance: Often overlooked but incredibly important. It protects your belongings from theft, fire, and other perils, and provides liability coverage if someone is injured in your rented space. It's usually very affordable.

- Disability Insurance: If you rely on your income, consider short-term and long-term disability insurance. It replaces a portion of your income if you become unable to work due to illness or injury.

Identity Theft Prevention Safeguarding Your Personal Information

In today's digital age, identity theft is a real threat. Protect yourself by:

- Using strong, unique passwords for all online accounts and enabling two-factor authentication.

- Being wary of phishing emails and suspicious links.

- Shredding sensitive documents before throwing them away.

- Regularly checking your bank and credit card statements for unauthorized activity.

- Considering a credit freeze if you're concerned about new accounts being opened in your name.

Financial Tools and Resources for Young Adults Apps and Websites to Help You Thrive

You don't have to navigate your financial journey alone. There are countless tools and resources designed to make financial planning easier and more accessible for young adults.

Budgeting Apps and Software Making Money Management Easy

These apps can automate expense tracking, categorize spending, and help you stick to your budget.

- Mint: Free, links all your accounts, tracks spending, creates budgets, and offers bill reminders.

- You Need A Budget (YNAB): A paid app with a cult following. It uses the zero-based budgeting method and is excellent for those who want to be very hands-on with their money.

- Personal Capital: Great for tracking net worth, investments, and overall financial health. Offers free tools and paid financial advisory services.

Financial Education Websites and Podcasts Learn and Grow

Continuously educate yourself. There are many free resources available:

- Investopedia: A comprehensive resource for all things investing and finance.

- NerdWallet: Offers reviews of financial products, budgeting advice, and financial guides.

- The Ramsey Show (Podcast): While some advice is controversial, it offers strong motivation for debt repayment.

- Afford Anything (Podcast): Focuses on financial independence and making intentional choices with your money.

Connecting with a Financial Advisor When to Seek Professional Guidance

While this guide provides a solid foundation, there might come a time when you need personalized advice. A financial advisor can help with complex investment strategies, estate planning, or navigating major life events. Look for a fee-only fiduciary advisor, meaning they are legally obligated to act in your best interest and are paid directly by you, not by commissions from selling products.

Your Financial Journey Starts Now Take Action and Stay Consistent

Financial planning isn't a one-time event; it's an ongoing journey. The most important thing is to start now, even if it's with small steps. Be consistent, review your progress regularly, and adjust your plan as your life and goals evolve. You'll make mistakes along the way, and that's okay. Learn from them, stay disciplined, and celebrate your successes. By taking control of your finances as a young adult, you're not just building wealth; you're building confidence, security, and the freedom to live the life you truly desire. Go forth and conquer your financial goals!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)