Snowball vs Avalanche Debt Payoff Methods

Compare the debt snowball and debt avalanche methods to find the most effective strategy for paying off your debts.

Compare the debt snowball and debt avalanche methods to find the most effective strategy for paying off your debts.

Snowball vs Avalanche Debt Payoff Methods Your Ultimate Guide to Crushing Debt

Hey there, debt slayer! Ready to finally kick those pesky debts to the curb? You've probably heard whispers about two popular debt payoff strategies: the debt snowball and the debt avalanche. Both are fantastic tools, but they tackle debt from slightly different angles. Think of it like this: one is a psychological powerhouse, and the other is a mathematical marvel. We're going to dive deep into both, compare them head-to-head, and even recommend some cool tools to help you on your journey. By the end of this, you'll be armed with all the knowledge you need to pick the perfect strategy for your financial freedom!

Understanding the Debt Snowball Method How it Works

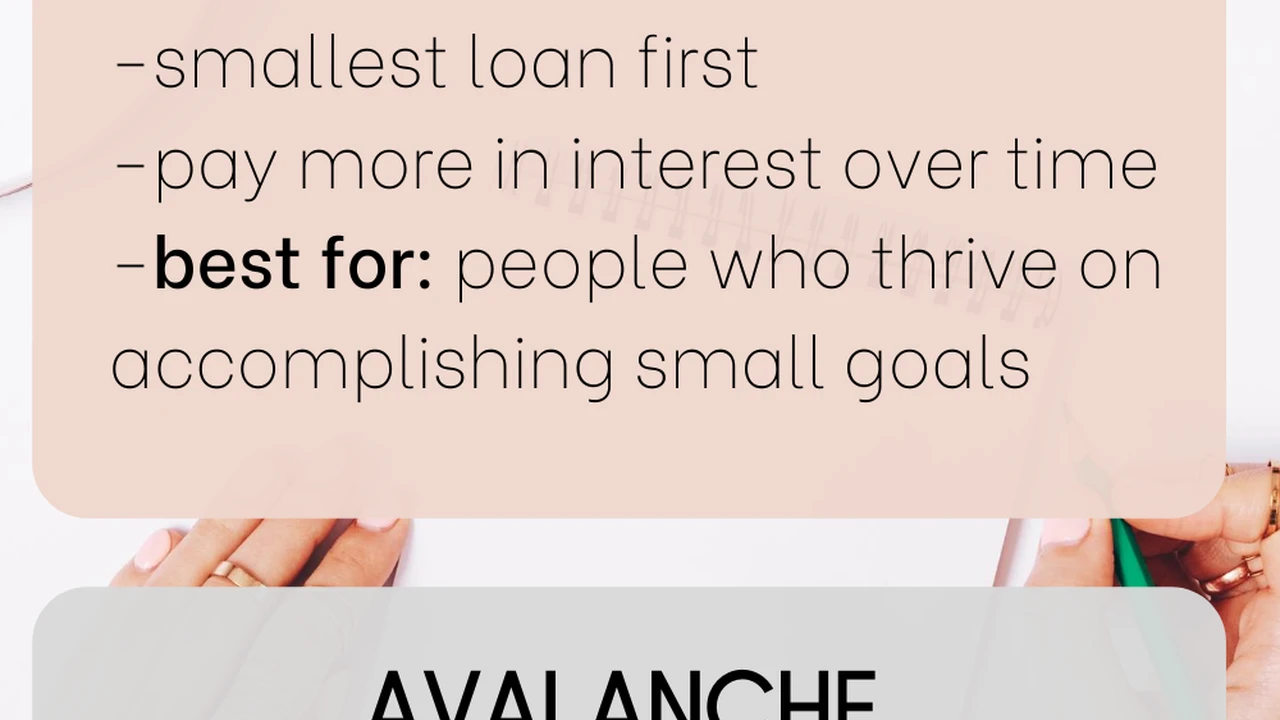

Let's start with the debt snowball. This method is all about momentum and motivation. It's championed by financial gurus like Dave Ramsey, and for good reason – it works wonders for people who need those small wins to stay on track. Here's the gist:

- List all your debts: Gather up every single debt you have – credit cards, personal loans, student loans, car loans, you name it.

- Order them by smallest balance: This is the crucial step. Ignore interest rates for a moment. Just list them from the smallest amount owed to the largest.

- Pay minimums on all but the smallest: For all your debts except the very smallest one, you'll pay just the minimum required payment.

- Attack the smallest debt: Throw every extra penny you can find at that smallest debt. Seriously, go all in! Cut back on lattes, pack your lunch, sell some old stuff – whatever it takes.

- Roll the payment: Once that smallest debt is gone (cue the confetti!), you take the money you were paying on it (the minimum payment plus all that extra you were throwing at it) and add it to the minimum payment of your next smallest debt. This is where the 'snowball' effect comes in. Your payments get bigger and bigger as you knock out each debt, gaining momentum like a snowball rolling downhill.

Why the Debt Snowball is a Motivational Powerhouse

The biggest advantage of the debt snowball is psychological. When you pay off that first small debt, it feels amazing! That sense of accomplishment fuels your motivation to keep going. It's like hitting a small target and then feeling confident enough to aim for bigger ones. For many people, especially those who feel overwhelmed by debt, these quick wins are essential to prevent burnout and keep them committed to their debt-free journey. It builds confidence and proves to yourself that you can do this.

Exploring the Debt Avalanche Method The Smartest Financial Play

Now, let's talk about the debt avalanche. If the debt snowball is about feelings, the debt avalanche is about pure, unadulterated math. This method is designed to save you the most money in interest over the long run. Here’s how it works:

- List all your debts: Just like with the snowball, get all your debts organized.

- Order them by highest interest rate: This is the key difference. You'll list your debts from the highest interest rate to the lowest, regardless of the balance.

- Pay minimums on all but the highest interest debt: Again, pay only the minimum required on all debts except the one with the highest interest rate.

- Attack the highest interest debt: Direct all your extra funds towards the debt with the highest interest rate. This is where your money will make the biggest impact in reducing the total amount you pay over time.

- Roll the payment: Once that highest interest debt is paid off, you take the money you were paying on it and add it to the minimum payment of your next highest interest debt. You continue this process until all your debts are gone.

Why the Debt Avalanche Saves You More Money

The debt avalanche is mathematically superior because it targets the most expensive debts first. By eliminating the debts that are costing you the most in interest, you reduce the total amount of money you pay back. Over time, this can translate into significant savings – sometimes thousands of dollars! If you're someone who is highly disciplined and motivated by saving money, the debt avalanche is likely your best bet.

Debt Snowball vs Debt Avalanche A Head-to-Head Comparison

So, which one is right for you? Let's break down the pros and cons to help you decide:

Debt Snowball Pros and Cons for Your Financial Journey

- Pros:

- High Motivation: Quick wins keep you engaged and prevent burnout.

- Psychological Boost: Seeing debts disappear provides a powerful sense of accomplishment.

- Simplicity: Easy to understand and implement, especially for beginners.

- Cons:

- More Interest Paid: You'll likely pay more in interest over the long run compared to the avalanche method.

- Slower Financial Savings: The financial benefits accumulate slower initially.

Debt Avalanche Pros and Cons for Maximum Savings

- Pros:

- Maximum Interest Savings: You save the most money on interest payments.

- Faster Debt-Free Date (Potentially): Because you're saving more on interest, you might become debt-free sooner, assuming consistent extra payments.

- Mathematically Efficient: The most financially sound approach.

- Cons:

- Less Immediate Motivation: If your highest interest debt is also your largest, it might take longer to see that first debt disappear, which can be demotivating for some.

- Requires Discipline: You need to be committed to the long game without the immediate gratification of small wins.

Choosing Your Debt Payoff Strategy Finding Your Fit

Ultimately, the 'best' method is the one you'll stick with. If you're someone who needs constant encouragement and visible progress to stay motivated, the debt snowball is probably your champion. If you're a numbers person, highly disciplined, and want to save every possible penny, the debt avalanche is your go-to. Some people even combine elements of both, starting with a small snowball to build momentum and then switching to an avalanche once they're feeling confident.

Consider your personality and your financial situation. Do you have a lot of small debts that you could quickly eliminate? Or do you have one or two really high-interest debts that are eating you alive? Be honest with yourself about what will keep you going when the going gets tough.

Tools and Apps to Help You Conquer Debt Your Digital Allies

No matter which method you choose, there are some fantastic tools and apps out there that can make your debt payoff journey smoother and more organized. These aren't just for tracking; they can help you visualize your progress, stay motivated, and even automate some of the heavy lifting.

1. Undebt.it The Free Debt Payoff Planner

What it is: Undebt.it is a free, web-based debt payoff planner that allows you to input all your debts and then choose between the snowball, avalanche, or even a custom method. It calculates your payoff date, total interest saved, and provides a visual representation of your progress. It's incredibly flexible and user-friendly.

Key Features:

- Supports both snowball and avalanche methods.

- Allows for custom payoff strategies.

- Visual progress tracking with charts and graphs.

- Email reminders for payments.

- Ability to add extra payments and see their impact.

- Completely free to use.

Use Case: Perfect for anyone who wants a comprehensive, free tool to plan and track their debt payoff. It's especially useful for comparing how much faster you could pay off debt and how much interest you could save by using one method over another. You can easily switch between strategies to see the financial implications.

Pricing: Free. There's a paid 'Plus' version for advanced features like syncing with bank accounts, but the core planning tools are free.

2. YNAB You Need A Budget The Budgeting Powerhouse

What it is: While primarily a budgeting app, YNAB (You Need A Budget) is an absolute game-changer for debt payoff because it helps you find the extra money to throw at your debts. It operates on a 'zero-based budgeting' philosophy, meaning every dollar has a job. This clarity helps you identify funds that can be redirected to debt.

Key Features:

- Zero-based budgeting system.

- Connects to bank accounts for automatic transaction import.

- Goal tracking, including debt payoff goals.

- Detailed reporting to see where your money is going.

- Excellent educational resources and community support.

Use Case: Ideal for individuals or families who need to get a firm grip on their spending to free up more money for debt payments. YNAB doesn't directly implement snowball or avalanche, but by helping you find more money, it supercharges whichever method you choose. It's about proactive money management.

Pricing: YNAB offers a 34-day free trial, then it's $14.99 per month or $99 per year. While it has a cost, many users find the savings it helps them achieve far outweigh the subscription fee.

3. Tally The Automated Debt Manager

What it is: Tally is a unique app that acts as an automated debt manager, specifically for credit card debt. It helps you pay down your credit cards more efficiently by offering a lower-interest line of credit to consolidate your high-interest balances. It then manages your payments, ensuring you pay on time and optimize your payoff strategy.

Key Features:

- Consolidates high-interest credit card debt into a single, lower-interest line of credit.

- Automates credit card payments, ensuring you never miss a due date.

- Optimizes payments to save you money on interest.

- Monitors your credit score and offers personalized advice.

- Can help you choose between snowball or avalanche-like strategies for your credit cards.

Use Case: Best for people with multiple credit cards carrying high interest rates who want an automated solution to manage and pay them down. If you struggle with making multiple payments or want to ensure you're always paying the optimal amount, Tally can be a lifesaver. It's particularly good for those who lean towards the avalanche method for credit cards but want help executing it.

Pricing: Tally's core service is free. If you qualify for their lower-interest line of credit, the interest rate will vary based on your creditworthiness (typically 7.99% to 29.99% APR). There are no annual fees for the Tally line of credit.

4. Debt Payoff Planner by Vertex42 The Spreadsheet Solution

What it is: For those who love spreadsheets and a hands-on approach, the Debt Payoff Planner by Vertex42 is an excellent Excel or Google Sheets template. It's a powerful, customizable spreadsheet that allows you to input all your debts, choose your payoff method (snowball or avalanche), and see detailed amortization schedules and payoff dates.

Key Features:

- Excel/Google Sheets based, offering full customization.

- Supports both snowball and avalanche methods.

- Calculates payoff dates and total interest paid.

- Allows for 'what-if' scenarios with extra payments.

- Provides a clear visual overview of your debt situation.

Use Case: Ideal for spreadsheet enthusiasts, those who prefer to keep their financial data offline, or anyone who wants a highly detailed and customizable view of their debt payoff plan. It's great for visualizing the impact of different payment strategies and extra payments.

Pricing: Free to download and use. It's a template, so you just need compatible spreadsheet software (like Microsoft Excel or Google Sheets, which is free).

5. Mint The All-in-One Financial Tracker

What it is: Mint is a popular free personal finance app that helps you track all your financial accounts in one place – bank accounts, credit cards, investments, and loans. While not solely a debt payoff tool, its comprehensive overview of your finances can be incredibly helpful in managing debt.

Key Features:

- Connects to all your financial accounts.

- Budgeting tools and spending categorization.

- Bill tracking and reminders.

- Credit score monitoring.

- Debt tracking, showing balances and interest rates.

Use Case: Great for people who want a holistic view of their financial health, including their debts. While it doesn't automate the snowball or avalanche, it provides the data you need to implement either strategy manually. It helps you see your overall financial picture, which is crucial for finding extra money to put towards debt.

Pricing: Free. Mint is ad-supported, but the core features are robust and free to use.

Real-World Scenarios Applying the Methods

Let's look at a couple of examples to see how these methods play out in real life. Imagine you have the following debts:

- Credit Card A: $500 balance, 24% interest, $25 minimum payment

- Personal Loan B: $2,000 balance, 10% interest, $50 minimum payment

- Student Loan C: $10,000 balance, 6% interest, $100 minimum payment

- Car Loan D: $15,000 balance, 4% interest, $250 minimum payment

And let's say you have an extra $100 per month to put towards debt.

Debt Snowball in Action Building Momentum

- Order by smallest balance:

- Credit Card A: $500

- Personal Loan B: $2,000

- Student Loan C: $10,000

- Car Loan D: $15,000

- Payments:

- Credit Card A: $25 (minimum) + $100 (extra) = $125

- Personal Loan B: $50 (minimum)

- Student Loan C: $100 (minimum)

- Car Loan D: $250 (minimum)

- Result: Credit Card A will be paid off very quickly (in about 4-5 months). Once it's gone, you'll take that $125 and add it to Personal Loan B's minimum payment. So, Personal Loan B will then receive $50 (minimum) + $125 (rolled from CC A) = $175 per month. This continues, and you get those satisfying wins along the way.

Debt Avalanche in Action Maximizing Savings

- Order by highest interest rate:

- Credit Card A: 24% ($500 balance)

- Personal Loan B: 10% ($2,000 balance)

- Student Loan C: 6% ($10,000 balance)

- Car Loan D: 4% ($15,000 balance)

- Payments:

- Credit Card A: $25 (minimum) + $100 (extra) = $125

- Personal Loan B: $50 (minimum)

- Student Loan C: $100 (minimum)

- Car Loan D: $250 (minimum)

- Result: Just like the snowball, Credit Card A gets paid off quickly because it has the highest interest rate and a small balance. However, if Personal Loan B had a higher interest rate than Credit Card A but a larger balance, the avalanche method would have you attacking Personal Loan B first, even if it took longer to pay off. The key is always targeting the highest interest rate. Once Credit Card A is gone, you'd roll that $125 to Personal Loan B, just like the snowball, but the initial targeting decision is based purely on interest rate.

Beyond the Methods Staying Debt-Free and Building Wealth

Paying off debt is a huge accomplishment, but it's just one step on your financial journey. Once you're debt-free, that extra money you were throwing at your debts can now be redirected to building wealth. Think about it: if you were paying an extra $500 a month towards debt, imagine what that $500 could do for your savings, investments, or retirement fund!

Building an Emergency Fund Your Financial Safety Net

Before you go wild investing, make sure you have a solid emergency fund. This is typically 3-6 months' worth of living expenses saved in an easily accessible account. An emergency fund prevents you from falling back into debt when unexpected expenses pop up, like a car repair or a medical bill. It's your financial shield.

Investing for Your Future Making Your Money Work

Once your emergency fund is solid, start investing! Whether it's contributing to a 401(k) or IRA, opening a brokerage account, or exploring real estate, investing allows your money to grow over time thanks to the magic of compound interest. The sooner you start, the more time your money has to multiply.

Continuous Financial Education Always Learning

The world of personal finance is always evolving. Keep learning about budgeting, investing, taxes, and wealth management. Read books, listen to podcasts, follow reputable financial blogs. The more you know, the better equipped you'll be to make smart financial decisions and maintain your debt-free status.

Final Thoughts on Your Debt Payoff Journey

Whether you choose the debt snowball or the debt avalanche, the most important thing is to choose a method and stick with it. Consistency and discipline are your best friends on this journey. Don't get discouraged if you hit a bump in the road; just get back on track. Celebrate your small victories, stay focused on your goal, and remember why you started this in the first place. You've got this, and financial freedom is well within your reach!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)