Impact of Late Payments on Your Credit Score

Understand the severe consequences of late payments on your credit score and how to avoid them for a healthier financial future.

Understand the severe consequences of late payments on your credit score and how to avoid them for a healthier financial future.

The Immediate Fallout How Late Payments Hit Your Credit Score

Let's face it, life happens. Sometimes, despite our best intentions, a bill slips through the cracks, or an unexpected expense throws our budget into disarray. Before you know it, that credit card payment or loan installment is past due. But what really happens when you make a late payment? It's not just a minor inconvenience; it can have a significant and lasting impact on your credit score, affecting your financial future in ways you might not immediately realize.

The first thing to understand is that a payment isn't typically considered 'late' by credit bureaus until it's 30 days past its due date. While your lender might charge you a late fee as soon as you miss the due date, they usually won't report it to the major credit bureaus (Experian, Equifax, and TransUnion) until that 30-day mark. This 30-day grace period is crucial. If you can make the payment within this window, even with a late fee, you can often prevent it from appearing on your credit report and damaging your score.

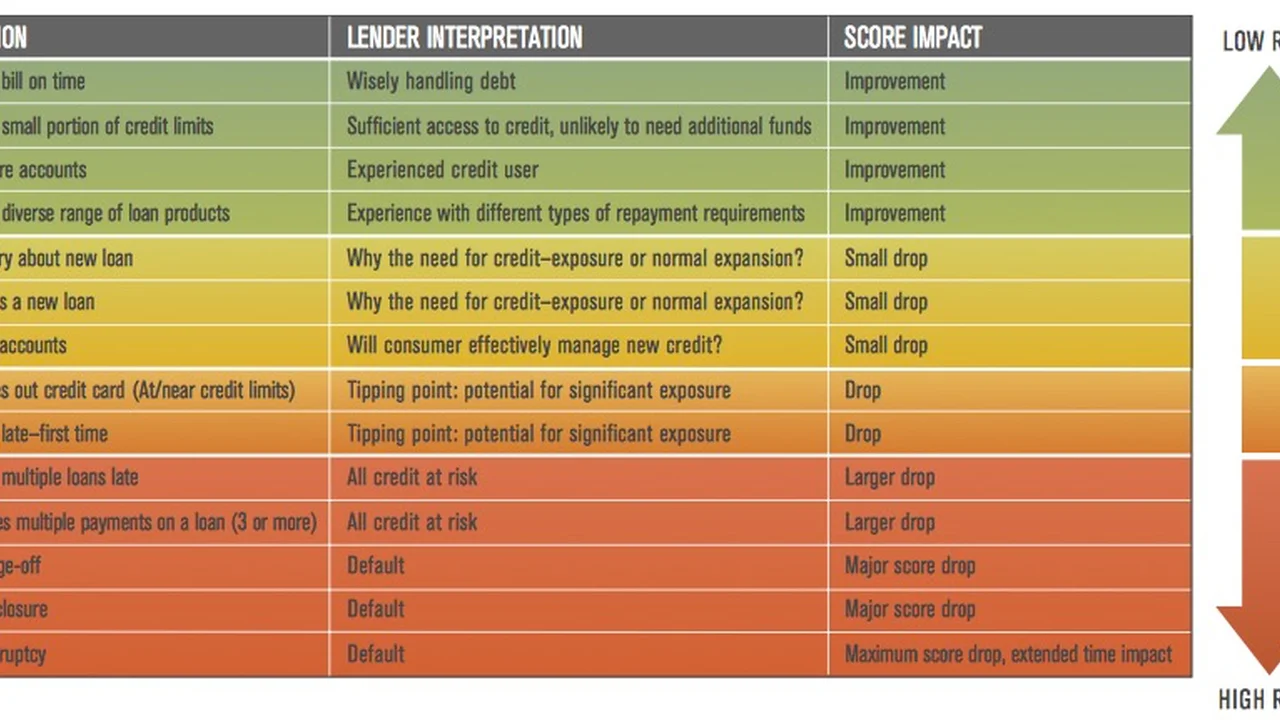

Once a payment is reported as 30 days late, the damage begins. Payment history is the single most important factor in calculating your FICO score, accounting for a whopping 35% of the total. A single 30-day late payment can cause a significant drop in your score, especially if you have an otherwise excellent credit history. The higher your score, the more it has to fall. For someone with a FICO score in the high 700s or 800s, a 30-day late payment could easily knock off 50 to 100 points. For someone with an already lower score, the drop might be less dramatic in terms of points, but it can still push them into a 'poor' credit category, making it even harder to access credit.

The severity of the impact also increases with the lateness. A 60-day late payment is worse than a 30-day late payment, and a 90-day late payment is even more detrimental. Each subsequent late payment on the same account will further erode your score. These negative marks can remain on your credit report for up to seven years, casting a long shadow over your financial endeavors.

Long Term Repercussions Beyond the Score Drop

The immediate drop in your credit score is just the beginning. The ripple effects of late payments can extend far and wide, impacting various aspects of your financial life for years to come.

Higher Interest Rates and Loan Denials Understanding the Cost of Lateness

One of the most direct consequences is the increased cost of borrowing. Lenders view late payments as a sign of higher risk. When you apply for a new loan or credit card, they'll see those late marks on your report and are likely to offer you higher interest rates, if they approve you at all. This means you'll pay more over the life of the loan for everything from mortgages and auto loans to personal loans and credit cards. For example, a difference of just a few percentage points on a mortgage can translate into tens of thousands of dollars in extra interest paid over 30 years. Imagine trying to get a competitive rate on a car loan with a recent 60-day late payment – it's going to be tough, and you'll likely end up paying significantly more.

Difficulty Renting and Insuring Your Future Housing and Coverage Impacts

It's not just about loans. Many landlords now check credit reports as part of their tenant screening process. A history of late payments can make it difficult to secure a rental property, especially in competitive markets. They want to see a reliable payment history, and late payments suggest you might not be a dependable tenant. Similarly, insurance companies, particularly for auto and home insurance, often use credit-based insurance scores to determine your premiums. A lower credit score due to late payments could mean you pay higher insurance rates, adding another financial burden.

Employment Opportunities and Background Checks Your Professional Image

Believe it or not, some employers, especially those in financial industries or positions of trust, may conduct credit checks as part of their background screening. While they can't see your actual credit score, they can see your credit report, including any late payments. A pattern of financial irresponsibility, as indicated by late payments, could potentially hinder your job prospects. It's not as common as other impacts, but it's a possibility to be aware of.

Credit Limit Reductions and Account Closures Lender Actions and Your Access to Credit

Existing creditors might also take action. If you consistently make late payments on a credit card, the issuer might reduce your credit limit or even close your account entirely. This not only makes it harder to access credit when you need it but can also negatively impact your credit utilization ratio (the amount of credit you're using compared to your total available credit), which is another important factor in your credit score.

Strategies to Avoid Late Payments Proactive Steps for Financial Health

The best defense against late payments is a good offense. Proactive strategies can help you stay on top of your bills and protect your credit score.

Automate Your Payments Set It and Forget It

This is perhaps the simplest and most effective strategy. Most banks and creditors offer automatic payment options. You can set up recurring payments from your checking account to cover your bills on their due dates. This eliminates the risk of forgetting a payment or missing it due to a busy schedule. Just make sure you have sufficient funds in your account to cover the payments to avoid overdraft fees and further financial headaches.

Product Recommendation: Most major banks like Chase, Bank of America, Wells Fargo, and Citibank offer robust online banking platforms with easy-to-use bill pay features. You can typically set up recurring payments for credit cards, loans, and even utilities directly through their websites or mobile apps. For example, with Chase, you can log into your account, navigate to 'Pay & Transfer,' and then 'Pay Bills' to set up automatic payments for various payees. These services are usually free for account holders.

Set Up Reminders and Alerts Your Digital Nudge

Even with automatic payments, it's a good idea to have reminders in place. Many credit card companies and lenders offer email or text message alerts that notify you a few days before a payment is due. You can also use calendar apps on your phone or computer to set up recurring reminders for all your bills. This provides an extra layer of protection against missed payments.

Product Recommendation:

- Mint (Free): A popular budgeting app that allows you to link all your financial accounts. It provides bill reminders, tracks your spending, and helps you create budgets. It's great for an overall financial snapshot and getting alerts for upcoming bills.

- Personal Capital (Free): Similar to Mint, Personal Capital offers a comprehensive view of your finances, including investment tracking and bill reminders. It's particularly strong for those with investments.

- Your Bank's Mobile App (Free with account): Most bank apps now offer customizable alerts for due dates, low balances, and payment confirmations. This is a convenient option if you prefer to keep everything within your primary banking ecosystem.

- Google Calendar / Apple Calendar (Free): Simple yet effective. You can set up recurring events for each bill with multiple reminders (e.g., 5 days before, 1 day before).

Create a Budget and Stick to It Your Financial Roadmap

A well-structured budget is fundamental to avoiding late payments. When you know exactly how much money is coming in and going out, you can allocate funds for all your bills and ensure you have enough to cover them. This helps prevent situations where you're short on cash when a payment is due. Regularly review your budget to make sure it aligns with your current income and expenses.

Product Recommendation:

- You Need A Budget (YNAB) ($14.99/month or $99/year): YNAB is a highly-regarded budgeting app that focuses on giving every dollar a job. It's excellent for proactive budgeting and ensuring you have money set aside for upcoming bills. It has a steeper learning curve but is incredibly powerful for financial control.

- Simplifi by Quicken ($3.99/month or $47.88/year): Simplifi offers a more streamlined approach to budgeting, focusing on tracking spending, creating spending plans, and monitoring subscriptions. It's user-friendly and provides good insights into your cash flow.

- Goodbudget (Free with paid upgrade options): Based on the envelope budgeting system, Goodbudget helps you allocate funds to different spending categories. It's great for couples or families who want to share a budget.

- Spreadsheets (Free): For those who prefer a DIY approach, a simple Google Sheet or Excel spreadsheet can be incredibly effective. You can customize it exactly to your needs. Many free templates are available online.

Consider Changing Due Dates Align with Your Pay Cycle

If your bill due dates consistently fall at an inconvenient time (e.g., before your paycheck arrives), contact your creditors and ask if you can change the due date. Many companies are willing to accommodate such requests, especially if you have a good payment history. Aligning due dates with your pay cycle can significantly reduce the stress of managing bills and the likelihood of missing a payment.

Build an Emergency Fund Your Financial Safety Net

An emergency fund is crucial for preventing late payments when unexpected expenses arise. Having three to six months' worth of living expenses saved in an easily accessible account (like a high-yield savings account) can be a lifesaver. If your car breaks down or you face a medical emergency, you can tap into your emergency fund instead of missing bill payments to cover the unexpected cost.

Product Recommendation:

- Ally Bank Online Savings Account (APY varies, typically competitive): Ally offers competitive interest rates, no monthly fees, and 24/7 customer service. It's a great option for parking your emergency fund.

- Discover Bank Online Savings Account (APY varies, typically competitive): Similar to Ally, Discover Bank provides high-yield savings accounts with no monthly fees and excellent customer service.

- Marcus by Goldman Sachs Online Savings Account (APY varies, typically competitive): Marcus is another strong contender for high-yield savings, known for its user-friendly interface and competitive rates.

What to Do If You've Already Made a Late Payment Damage Control and Recovery

If you've already made a late payment, don't despair. While you can't erase it from your credit history immediately, there are steps you can take to mitigate the damage and start rebuilding your credit.

Pay the Overdue Amount Immediately Stop the Bleeding

The first and most critical step is to pay the overdue amount as soon as possible. The longer a payment is late (30, 60, 90+ days), the more severe the impact on your credit score. Getting current on your payments prevents further damage and shows creditors you're taking responsibility.

Contact Your Creditor Explain and Negotiate

Once you've made the payment, contact your creditor. Explain the situation honestly and politely. If this is your first late payment, or if you have a long history of on-time payments, you might be able to ask for a 'goodwill adjustment.' This is where the creditor agrees to remove the late payment mark from your credit report as a gesture of goodwill. It's not guaranteed, but it's worth a try, especially if you're a valued customer. Be prepared to explain why the payment was late and what steps you've taken to prevent it from happening again.

Monitor Your Credit Report For Accuracy and Progress

Regularly check your credit reports from all three major bureaus (Experian, Equifax, and TransUnion) to ensure the late payment is reported accurately. If you successfully negotiated a goodwill adjustment, verify that the late payment has indeed been removed. You can get a free copy of your credit report from each bureau once a year at AnnualCreditReport.com.

Product Recommendation:

- AnnualCreditReport.com (Free): The only government-authorized website for free credit reports from all three bureaus. You can access one report from each bureau annually.

- Credit Karma (Free): Provides free credit scores (VantageScore) and reports from TransUnion and Equifax. It also offers credit monitoring and alerts for changes to your report.

- Experian, Equifax, TransUnion (Free basic monitoring, paid upgrades): Each bureau offers free access to your credit score and report, along with paid services for more in-depth monitoring and identity theft protection.

Focus on Consistent On-Time Payments Rebuilding Your History

The most effective way to recover from a late payment is to establish a consistent pattern of on-time payments going forward. Every on-time payment you make after a late one helps to dilute its negative impact over time. The further in the past the late payment is, and the more positive payment history you accumulate, the less weight it will carry in your credit score calculation.

Consider a Secured Credit Card or Credit Builder Loan For Active Rebuilding

If your credit score has taken a significant hit, and you're struggling to get approved for traditional credit, consider a secured credit card or a credit builder loan. These products are designed to help individuals rebuild their credit by demonstrating responsible payment behavior. A secured credit card requires a cash deposit as collateral, which typically becomes your credit limit. A credit builder loan works in reverse: you make payments into a savings account, and once the loan is paid off, you receive the funds. Both report your payments to the credit bureaus, helping you establish a positive payment history.

Product Recommendation:

- Discover it Secured Credit Card (No annual fee, requires security deposit): A popular choice for rebuilding credit, offering cash back rewards and a path to an unsecured card.

- Capital One Platinum Secured Credit Card (No annual fee, requires security deposit): Another solid option with flexible security deposit requirements.

- Self Lender Credit Builder Account (Fees apply, varies by loan amount): Self Lender offers credit builder loans that help you save money while building credit. They report to all three major credit bureaus.

- Kikoff Credit Account (Free for basic account, paid for premium features): Kikoff offers a small line of credit that helps build payment history without a hard credit check.

Understanding the Nuances Different Types of Late Payments

It's also important to understand that not all late payments are created equal in the eyes of credit bureaus and lenders.

Credit Card Late Payments High Impact

Late payments on credit cards tend to have a very high impact on your credit score because credit cards are revolving credit, and consistent, on-time payments are a key indicator of responsible credit management.

Loan Late Payments Mortgages Auto Personal

Late payments on installment loans like mortgages, auto loans, and personal loans also carry significant weight. A late mortgage payment, in particular, can be very damaging due to the large sums involved and the importance of housing stability.

Utility and Cell Phone Bills Less Direct Impact

Generally, late payments on utility bills (electricity, water, gas) or cell phone bills do not directly impact your credit score unless the account goes into collections. If a utility company sends your unpaid bill to a collection agency, that collection account will then appear on your credit report and severely damage your score. So, while a single late utility payment might not show up, letting it go unpaid for too long can lead to serious credit problems.

Medical Bills Similar to Utilities

Similar to utilities, medical bills typically don't appear on your credit report unless they are sent to collections. However, new rules are making it less likely for medical debt under $500 to appear on credit reports, and paid medical collections are being removed. Still, it's best to address medical bills promptly to avoid them going to collections.

Final Thoughts on Protecting Your Credit

The impact of late payments on your credit score is undeniable and can have far-reaching consequences. By understanding how they affect your score, implementing proactive strategies to avoid them, and knowing how to mitigate the damage if one occurs, you can protect your financial health. Remember, consistency is key when it comes to credit. Every on-time payment you make builds a stronger foundation for your financial future, opening doors to better interest rates, easier approvals, and greater financial freedom. Stay vigilant, stay organized, and prioritize your payments to keep your credit score in excellent shape.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)