Learn how loan amortization schedules work and how they impact your monthly payments and total interest paid.

Learn how loan amortization schedules work and how they impact your monthly payments and total interest paid. Ever wondered how your loan payments are calculated, or why you pay so much interest at the beginning of a loan term? It all comes down to something called an amortization schedule. This isn't just some fancy financial term; it's a crucial tool that breaks down every single payment you'll make on a loan, showing you exactly how much goes towards the principal (the original amount you borrowed) and how much goes towards interest. Understanding this can save you a ton of money and help you make smarter financial decisions, whether you're taking out a mortgage, a car loan, or even a personal loan.

Understanding Loan Amortization Schedules

What is Loan Amortization and Why Does it Matter?

So, what exactly is amortization? In simple terms, it's the process of paying off a debt over time through regular, equal payments. Each payment consists of two parts: a portion that reduces the principal balance of the loan and a portion that covers the interest accrued since the last payment. An amortization schedule is essentially a table that details each of these payments, showing the date, the payment amount, the interest paid, the principal paid, and the remaining balance after each payment. It's like a roadmap for your loan.

Why does this matter to you? Well, for starters, it provides transparency. You'll know exactly where your money is going with every payment. More importantly, it reveals a key characteristic of most amortized loans: in the early stages, a larger percentage of your payment goes towards interest, and a smaller portion goes towards the principal. As the loan matures, this ratio gradually shifts, with more of your payment chipping away at the principal. This is a critical concept to grasp, especially if you're considering making extra payments or refinancing.

How Loan Amortization Works The Mechanics Behind Your Payments

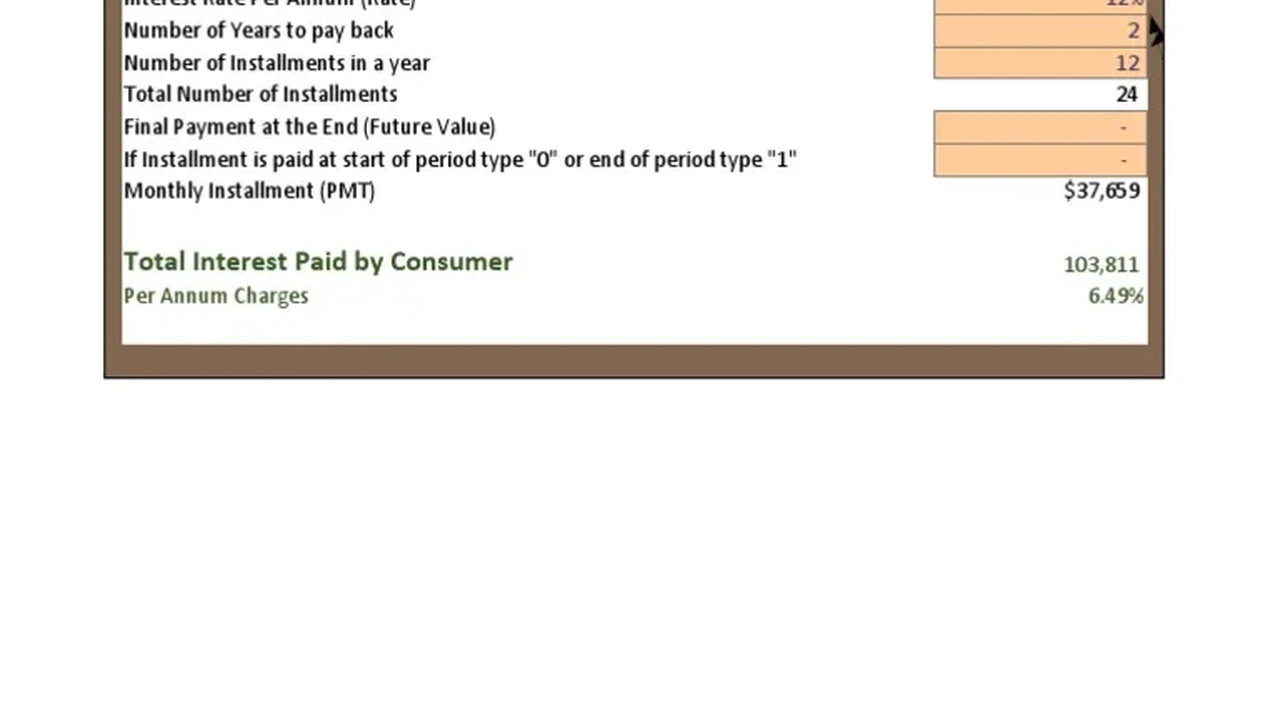

Let's dive a bit deeper into the mechanics. The calculation of an amortized loan payment is based on a few key variables: the principal loan amount, the interest rate, and the loan term (the number of payments). Lenders use a specific formula to determine a fixed monthly payment that will fully pay off the loan, including all interest, by the end of the term. This fixed payment ensures predictability for borrowers, but the internal breakdown of principal and interest changes over time.

Imagine you take out a $100,000 mortgage at 4% interest over 30 years. Your monthly payment might be around $477. But in the first month, a significant chunk of that $477 will be interest, perhaps $333, leaving only $144 to reduce your principal. Fast forward 15 years, and your payment is still $477, but now maybe only $150 is interest, and $327 goes to principal. This front-loading of interest is standard practice and is why paying extra early on can have such a dramatic impact on the total interest you pay over the life of the loan.

Key Components of an Amortization Schedule Understanding Each Column

An amortization schedule typically includes several columns, each providing vital information:

* Payment Number: This simply indicates which payment you're making in the sequence (e.g., 1st, 2nd, 3rd, etc.).

* Payment Date: The scheduled date for each payment.

* Beginning Balance: The outstanding principal balance at the start of the payment period.

* Scheduled Payment: The fixed amount you are required to pay each period.

* Interest Paid: The portion of your payment that covers the interest accrued on the outstanding balance since the last payment.

* Principal Paid: The portion of your payment that directly reduces your loan's principal balance.

* Ending Balance: The remaining principal balance after the current payment has been applied.

* Cumulative Interest: Sometimes included, this column tracks the total interest paid up to that point.

By looking at these columns, you can clearly see the gradual shift from interest-heavy payments to principal-heavy payments. It's a powerful visual representation of your loan's progress.

The Impact of Interest Rates and Loan Terms on Amortization

Interest rates and loan terms are two of the biggest factors influencing your amortization schedule and, ultimately, the total cost of your loan. Let's break it down:

* Interest Rate: A higher interest rate means a larger portion of each payment will go towards interest, especially in the early years. This increases the total amount of interest you'll pay over the life of the loan. Even a small difference in interest rates can translate to thousands of dollars over a long loan term. For example, a $200,000, 30-year mortgage at 4% has a total interest cost of about $143,739. At 5%, that jumps to $186,512 – a difference of over $40,000!

* Loan Term: A longer loan term (e.g., 30 years vs. 15 years for a mortgage) results in lower monthly payments, which can be attractive for budgeting. However, it also means you'll pay significantly more in total interest because you're stretching out the repayment period and giving interest more time to accrue. Conversely, a shorter loan term means higher monthly payments but substantially less total interest paid. A 15-year mortgage on that same $200,000 at 4% would have a total interest cost of about $66,000 – a massive saving compared to the 30-year option.

Understanding this interplay is crucial when you're shopping for a loan. Don't just look at the monthly payment; consider the total cost of the loan over its lifetime.

Amortization for Different Loan Types Mortgages Auto Loans Personal Loans

While the core concept of amortization remains the same, its application can look slightly different across various loan types:

Mortgage Amortization The Long Haul

Mortgages are perhaps the most common example of amortized loans. Due to their large principal amounts and long terms (15, 20, or 30 years), the front-loading of interest is very pronounced. In the first few years of a 30-year mortgage, you might be paying 70-80% interest and only 20-30% principal. This is why making extra principal payments on a mortgage can be incredibly effective in reducing the total interest paid and shortening the loan term. Many homeowners use amortization calculators to see the impact of even a small extra payment each month.

Auto Loan Amortization Faster Payoff

Auto loans typically have shorter terms (3 to 7 years) and smaller principal amounts than mortgages. While the interest is still front-loaded, the effect is less dramatic and the shift to principal-heavy payments happens much faster. An amortization schedule for an auto loan will show you how quickly you build equity in your vehicle, assuming its value doesn't depreciate faster than you pay it off. Knowing this can help you decide when it might be a good time to trade in or sell your car.

Personal Loan Amortization Flexible Terms

Personal loans can have a wide range of terms, from a few months to several years, and interest rates can vary significantly based on your creditworthiness. The amortization schedule for a personal loan will clearly show you how quickly you're paying down the debt and the total interest cost. This is particularly useful if you're using a personal loan for debt consolidation, as it allows you to track your progress towards becoming debt-free.

Strategies to Optimize Your Amortization Schedule Save Money and Pay Off Faster

Understanding your amortization schedule isn't just academic; it's a powerful tool for saving money and achieving financial freedom faster. Here are some strategies you can employ:

Making Extra Principal Payments The Power of Early Action

This is arguably the most effective strategy. Because interest is calculated on your outstanding principal balance, any extra money you pay directly towards the principal reduces that balance immediately. This means less interest accrues in subsequent periods, and more of your future payments go towards principal. Even small, consistent extra payments can shave years off a mortgage and save you tens of thousands of dollars in interest. For example, paying an extra $100 per month on a $200,000, 30-year mortgage at 4% could save you over $20,000 in interest and cut nearly 4 years off your loan term.

Bi-Weekly Payments A Simple Trick

Instead of making one monthly payment, consider making half of your payment every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, which equates to 13 full monthly payments per year instead of 12. That extra payment each year goes directly towards principal, significantly accelerating your payoff and reducing total interest. Many lenders offer this option, or you can simply make an extra principal payment once a year.

Refinancing Your Loan Lower Rates Shorter Terms

If interest rates have dropped since you took out your loan, or if your credit score has significantly improved, refinancing could be a smart move. By securing a lower interest rate, you'll reduce the total interest paid over the life of the loan. You could also choose to refinance into a shorter loan term (e.g., from 30 years to 15 years) to pay off the loan much faster, though this will result in higher monthly payments. Always compare the total cost of the new loan, including closing costs, against the savings.

Avoiding Interest-Only Payments The Long-Term Trap

Some loans, particularly certain types of mortgages or lines of credit, offer interest-only payment periods. While these can provide temporary relief with lower monthly payments, they are generally not advisable for long-term financial health. During an interest-only period, your principal balance doesn't decrease, meaning you're not building equity and you'll pay significantly more interest over the life of the loan once principal payments begin. It's a short-term gain for a long-term pain.

Tools and Resources for Amortization Calculation Online Calculators and Software

You don't need to be a math whiz to understand your amortization schedule. There are plenty of excellent tools available to help you visualize and calculate your loan payments:

Online Amortization Calculators Free and Easy to Use

Many financial websites offer free online amortization calculators. These are incredibly user-friendly. You simply input your loan amount, interest rate, and loan term, and the calculator instantly generates a full amortization schedule. Some popular options include:

* Bankrate Amortization Calculator: A very comprehensive and easy-to-use calculator that allows you to see the impact of extra payments.

* Mortgage Calculator.org: Offers detailed amortization schedules for various loan types, including options for additional payments.

* NerdWallet Amortization Calculator: Provides clear breakdowns and visual graphs to help you understand your loan.

These calculators are fantastic for planning and seeing the 'what if' scenarios, like how much you'd save by paying an extra $50 a month.

Spreadsheet Software Excel Google Sheets for Customization

If you're comfortable with spreadsheets, you can create your own amortization schedule in Microsoft Excel or Google Sheets. This gives you maximum flexibility to customize the schedule, add different payment scenarios, and track your actual payments against the plan. There are many free templates available online that you can adapt. This method is great for those who like to have full control and want to perform more complex analyses.

Loan Servicer Portals Your Personal Schedule

Most loan servicers (the company you make payments to) provide access to your specific amortization schedule through their online portals. This is your actual, personalized schedule based on your loan terms. It's a good idea to review this periodically to ensure accuracy and to track your progress.

Common Misconceptions About Loan Amortization Debunked

There are a few common misunderstandings about amortization that can lead to poor financial decisions. Let's clear them up:

Myth 1 My Monthly Payment is Mostly Principal Early On

As we've discussed, this is generally false for most amortized loans, especially long-term ones like mortgages. The vast majority of your early payments go towards interest. Understanding this is key to realizing the power of extra principal payments.

Myth 2 All Loans Amortize the Same Way

While the principle is similar, the specific amortization schedule varies greatly depending on the loan type, interest rate, and term. A credit card, for instance, is a revolving line of credit and doesn't have a fixed amortization schedule in the same way a mortgage does. Its minimum payment calculation is different and often leads to paying interest indefinitely if only minimums are made.

Myth 3 Paying Extra Only Helps at the End of the Loan

Quite the opposite! Paying extra principal at the beginning of a loan has the most significant impact because it reduces the principal balance on which future interest is calculated. This compound effect saves you more money over the long run than making extra payments later in the loan term.

The Bottom Line Empowering Your Financial Decisions

Understanding loan amortization schedules isn't just about numbers; it's about empowering yourself to make smarter financial decisions. By knowing how your payments are allocated between principal and interest, you can strategically tackle your debt, save money, and achieve your financial goals faster. Whether you're planning to buy a home, a car, or consolidate debt, taking the time to review and understand your amortization schedule is a crucial step towards financial literacy and success. So go ahead, pull up an amortization calculator, plug in your numbers, and see the power of this financial tool for yourself. It's your money, and knowing where it goes is the first step to taking control.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)