The Ultimate Guide to Credit Score Ranges

Demystify credit score ranges from excellent to poor and understand what each tier means for your financial opportunities.

Demystify credit score ranges from excellent to poor and understand what each tier means for your financial opportunities.

The Ultimate Guide to Credit Score Ranges

Hey there! Ever wondered what those three-digit numbers, your credit score, actually mean? It's not just a random number; it's a powerful indicator of your financial health, influencing everything from getting a new credit card to buying a house. Understanding credit score ranges is super important because it helps you know where you stand and what steps you might need to take to improve your financial future. Let's dive deep into what these ranges are, what they signify, and how you can navigate them.

Understanding Credit Score Basics What is a Credit Score?

Before we break down the ranges, let's quickly recap what a credit score is. In a nutshell, a credit score is a numerical representation of your creditworthiness. Lenders use it to assess the risk of lending you money. The higher your score, the less risky you appear to lenders, which usually translates to better interest rates and more favorable loan terms. The most common credit scoring models are FICO and VantageScore, and while they use slightly different methodologies, their core purpose is the same.

FICO Score Ranges Decoding Your Financial Health

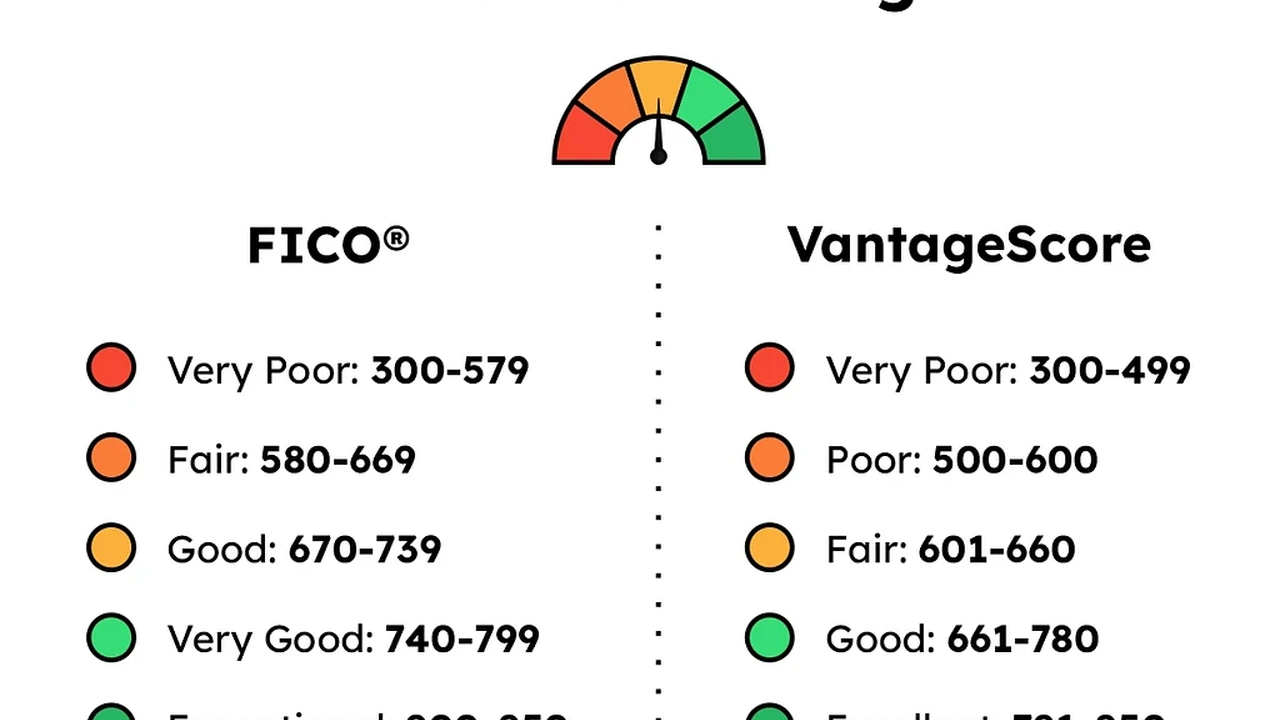

FICO scores are the most widely used credit scores by lenders, with about 90% of top lenders relying on them. FICO scores typically range from 300 to 850. Here's a breakdown of what each range generally means:

Excellent Credit Score 800-850 The Financial Elite

If your FICO score falls into this range, congratulations! You're in the financial elite. People with excellent credit scores are seen as extremely low-risk borrowers. This means you'll qualify for the best interest rates on loans, premium credit cards with fantastic rewards, and generally have an easier time getting approved for almost any financial product. Lenders will practically be rolling out the red carpet for you. You've demonstrated a long history of responsible credit management, including timely payments, low credit utilization, and a diverse credit mix.

Very Good Credit Score 740-799 Strong and Reliable

A very good credit score is still fantastic and puts you in a strong position. You'll still qualify for excellent interest rates and favorable terms on most loans and credit cards. While not quite at the top tier, lenders view you as a very reliable borrower. Maintaining a score in this range shows consistent financial responsibility. You might not get every single 'best-of-the-best' offer, but you'll be very close.

Good Credit Score 670-739 Solid and Dependable

This is where the majority of Americans fall, and it's a solid, dependable range. With a good credit score, you'll generally be approved for most loans and credit cards, though the interest rates might be slightly higher than those with excellent or very good credit. It indicates that you're a responsible borrower, but there might be a few minor blemishes or a shorter credit history compared to higher tiers. It's a great foundation to build upon.

Fair Credit Score 580-669 Room for Improvement

A fair credit score means you're likely to be approved for credit, but you'll probably face higher interest rates and less attractive terms. Lenders see you as a moderate risk. This range often indicates some past credit issues, such as late payments or higher credit utilization. While it's not ideal, it's definitely not the end of the world, and there's plenty of room for improvement. You might need to work a bit harder to get approved for certain products.

Poor Credit Score 300-579 High Risk, High Cost

If your FICO score is in this range, lenders consider you a high-risk borrower. Getting approved for traditional loans or credit cards will be challenging, and if you are approved, the interest rates will be very high. This range usually reflects a history of significant credit problems, such as bankruptcies, foreclosures, or numerous late payments and collections. It's a tough spot to be in, but it's absolutely possible to improve your score from here with consistent effort and smart financial decisions.

VantageScore Ranges Another Perspective on Creditworthiness

VantageScore is another popular credit scoring model, developed by the three major credit bureaus (Experian, Equifax, and TransUnion). Like FICO, VantageScores also range from 300 to 850, but their categorization of ranges can be slightly different. It's good to be aware of both, as some lenders might use one over the other.

VantageScore Excellent 781-850 Top Tier Access

Similar to FICO's excellent range, this score means you have top-tier access to the best financial products and rates. You're seen as an exceptionally reliable borrower.

VantageScore Good 661-780 Solid Opportunities

This range is broader than FICO's 'good' category and still offers solid opportunities for favorable loan terms and credit card approvals. You're considered a responsible borrower.

VantageScore Fair 601-660 Moderate Risk

In this range, you'll likely qualify for credit, but with higher interest rates and potentially less attractive terms. Lenders see you as a moderate risk, similar to FICO's fair category.

VantageScore Poor 500-600 Challenging Approvals

This range indicates significant credit challenges. Approvals will be difficult, and interest rates will be high. It's a clear signal that credit repair is needed.

VantageScore Very Poor 300-499 High Risk, Limited Options

The lowest tier, signifying very high risk. Options for credit will be extremely limited and costly. This range often points to severe credit issues.

Why Your Credit Score Range Matters Real World Impact

Understanding your credit score range isn't just academic; it has real-world implications for your financial life. Here's how it can affect you:

Loan Approvals and Interest Rates Saving Money on Loans

This is perhaps the most direct impact. A higher credit score range means you're more likely to be approved for loans (mortgages, auto loans, personal loans) and, crucially, you'll get lower interest rates. Over the life of a loan, even a small difference in interest rate can save you thousands, or even tens of thousands, of dollars. For example, someone with an excellent credit score might get a mortgage interest rate of 3%, while someone with a fair score might get 5% or more. On a $300,000 mortgage, that's a huge difference in total payments.

Credit Card Offers Rewards and Benefits

Premium credit cards with lucrative rewards programs (cash back, travel points, sign-up bonuses) are typically reserved for individuals with very good to excellent credit. If your score is lower, you might only qualify for basic cards with fewer benefits or even secured credit cards, which require a deposit. A good score opens doors to better perks and more financial flexibility.

Renting an Apartment Landlord Scrutiny

Many landlords check credit scores as part of their tenant screening process. A low score might make it harder to rent an apartment, or you might be required to pay a larger security deposit or have a co-signer. Landlords want to ensure you're reliable and will pay your rent on time.

Insurance Premiums Potential Savings

In many states, insurance companies use credit-based insurance scores to help determine your premiums for auto and home insurance. A higher credit score can lead to lower insurance rates, saving you money on essential coverage.

Utility Services Deposits and Connections

Some utility companies (electricity, gas, water) might check your credit score before connecting services. If you have a low score, they might require a security deposit, which can be an unexpected upfront cost.

Employment Opportunities Background Checks

While less common for all jobs, certain positions, especially those involving financial responsibilities or access to sensitive information, may involve a credit check. Employers aren't looking at your score directly but rather your credit report for signs of financial instability or irresponsibility. A poor credit history could be a red flag.

Factors Influencing Your Credit Score Understanding the Drivers

Your credit score isn't static; it's a dynamic number influenced by several key factors. Understanding these can help you improve your score and move into a better range:

Payment History The Biggest Impact

This is the most crucial factor, accounting for about 35% of your FICO score. Paying your bills on time, every time, is paramount. Late payments, collections, bankruptcies, and foreclosures can severely damage your score. Even one late payment can have a noticeable negative effect.

Credit Utilization Ratio How Much You Owe

This factor accounts for about 30% of your FICO score. It's the amount of credit you're using compared to your total available credit. Keeping your credit utilization below 30% (and ideally even lower, like 10%) is recommended. For example, if you have a credit card with a $10,000 limit, try to keep your balance below $3,000. High utilization signals to lenders that you might be over-reliant on credit.

Length of Credit History Time is Money

This makes up about 15% of your FICO score. Lenders like to see a long history of responsible credit use. The longer your accounts have been open and in good standing, the better. This is why it's often advised not to close old credit accounts, even if you don't use them much, as it shortens your average account age.

Credit Mix Types of Credit

About 10% of your FICO score comes from your credit mix. This refers to having a healthy variety of credit accounts, such as installment loans (mortgages, auto loans) and revolving credit (credit cards). It shows you can manage different types of debt responsibly. However, don't open new accounts just to diversify; let it happen naturally as your financial needs evolve.

New Credit Applications and Inquiries

This accounts for about 10% of your FICO score. When you apply for new credit, a 'hard inquiry' is placed on your credit report, which can temporarily ding your score. A few inquiries over a short period are usually fine, but too many can signal to lenders that you're desperate for credit or taking on too much debt. 'Soft inquiries,' like checking your own credit score, don't affect your score.

Strategies for Improving Your Credit Score Moving Up the Ranks

No matter where your credit score currently stands, there are always steps you can take to improve it. Moving into a higher range can unlock significant financial benefits.

Pay Bills On Time Every Time The Golden Rule

Seriously, this is the most important thing you can do. Set up automatic payments, calendar reminders, or whatever it takes to ensure you never miss a payment. Even one late payment can set you back.

Keep Credit Utilization Low Manage Your Debt

Aim to keep your credit card balances well below 30% of your available credit. If you have multiple cards, try to keep each one low. Paying down balances is a quick way to see your score improve.

Review Your Credit Report Regularly Spot Errors

You're entitled to a free credit report from each of the three major bureaus (Experian, Equifax, TransUnion) once a year via AnnualCreditReport.com. Check them for errors or fraudulent activity. Disputing inaccuracies can help boost your score.

Don't Close Old Accounts Maintain History

As mentioned, the length of your credit history matters. Closing old, paid-off accounts can shorten your average account age and negatively impact your score. Keep them open, even if you only use them occasionally.

Become an Authorized User Boost from Others

If someone with excellent credit (like a parent or trusted partner) adds you as an authorized user on their credit card, their positive payment history can appear on your credit report, potentially boosting your score. Just make sure they are financially responsible!

Consider a Secured Credit Card Building from Scratch

If you have poor or no credit, a secured credit card can be a great tool. You put down a deposit, which becomes your credit limit. This helps you build a positive payment history without much risk to the lender. After a period of responsible use, you might graduate to an unsecured card.

Credit Builder Loans A Structured Approach

These are small loans designed specifically to help you build credit. The loan amount is held in a savings account while you make payments. Once the loan is paid off, you get access to the money, and your positive payment history is reported to credit bureaus.

Credit Score Monitoring Services Keeping an Eye on Your Numbers

Staying on top of your credit score is crucial. Several services can help you monitor your score and report, often for free. While these services might use VantageScore or a FICO score variant, they provide valuable insights and alerts.

Credit Karma Free VantageScore Monitoring

Credit Karma is a very popular free service that provides your VantageScore 3.0 from TransUnion and Equifax. It also offers credit monitoring, alerts for changes, and personalized recommendations for credit cards and loans. It's a great tool for general credit health awareness.

Credit Sesame Free Credit Score and Monitoring

Similar to Credit Karma, Credit Sesame offers a free VantageScore and credit monitoring. It also provides insights into your debt and suggestions for improving your financial standing. They often highlight factors impacting your score and offer advice on how to address them.

Experian Free FICO Score and Report

Experian offers a free FICO Score 8 and a free Experian credit report. This is particularly valuable because FICO scores are so widely used by lenders. You can also get alerts for changes to your Experian report. This is a must-have for anyone serious about monitoring their FICO score directly.

MyFICO Paid FICO Score Access

While Experian offers one free FICO score, MyFICO is the official consumer division of FICO and offers access to all your FICO scores (there are many different versions for different types of lending) from all three bureaus. This is a paid service, but it's the most comprehensive way to see the exact FICO scores lenders are using. They offer various plans, typically ranging from $19.95 to $39.95 per month, depending on the level of detail and frequency of updates you need.

Specific Products to Consider for Credit Building and Repair

Let's talk about some concrete products that can help you build or rebuild your credit, along with some comparisons and typical costs.

Secured Credit Cards Best for Bad or No Credit

These cards require a security deposit, which typically becomes your credit limit. They are excellent for people with no credit history or those looking to rebuild after financial setbacks. The key is to use them responsibly and pay on time.

Product Comparison and Pricing:

- Discover it Secured Credit Card: Often considered one of the best. Requires a minimum deposit of $200. Offers 2% cash back at gas stations and restaurants on up to $1,000 in combined purchases each quarter, and 1% cash back on all other purchases. No annual fee. Discover also reviews your account after 7 months to see if you qualify to graduate to an unsecured card and get your deposit back.

- Capital One Platinum Secured Credit Card: Offers flexible security deposit options ($49, $99, or $200 for a $200 credit line). No annual fee. Capital One also offers a path to a higher credit line with responsible use, and eventually, graduation to an unsecured card.

- OpenSky Secured Visa Credit Card: No credit check required for approval, making it accessible for those with very poor credit. Requires a minimum deposit of $200. It has an annual fee of $35. This card is a good option if you've been turned down elsewhere due to your credit history.

Typical Cost: The main cost is the security deposit (fully refundable if you close the account in good standing) and potentially a small annual fee. Interest rates can be high if you carry a balance, but the goal is to pay in full each month.

Credit Builder Loans Structured Savings and Credit Building

These loans are designed to help you save money and build credit simultaneously. The loan amount is held in a locked savings account, and you make monthly payments. Once paid off, you get the money, and your payments are reported to credit bureaus.

Product Comparison and Pricing:

- Self Credit Builder Account: Offers loans ranging from $500 to $2,500. You make monthly payments (e.g., $25-$150) over 12-24 months. Once paid off, you get the money. They also offer a secured credit card option after a few months of on-time payments. Fees include an administrative fee (e.g., $9-$15) and interest on the loan (e.g., 15-16% APR, but you get the principal back).

- Kikoff Credit Account: This is a unique product that offers a 'credit line' to purchase items from their store (e.g., digital financial literacy products). You make small monthly payments (e.g., $5-$10), and these payments are reported to credit bureaus. It's a very low-cost way to build payment history. No annual fee, no interest if you pay on time.

- SeedFi Credit Builder Prime: Similar to Self, SeedFi offers a credit builder loan where you save money and build credit. They also have a 'Borrow & Grow' plan that combines a small immediate loan with a credit builder savings component. Fees and interest rates are comparable to Self.

Typical Cost: You'll pay a small administrative fee and some interest, but you get the principal amount back at the end. The cost is essentially the fee and interest paid for the service of building credit and forced savings.

Personal Loans for Debt Consolidation or Large Purchases

If you have a fair to good credit score, a personal loan can be a good option for consolidating high-interest debt or financing a large purchase. They offer fixed payments and a clear payoff schedule.

Product Comparison and Pricing:

- LightStream Personal Loans: Known for offering some of the lowest interest rates for borrowers with excellent credit (700+ FICO). They offer loans from $5,000 to $100,000 with terms from 24 to 84 months. APRs can start as low as 6-7% for excellent credit. No fees.

- SoFi Personal Loans: Caters to borrowers with good to excellent credit (typically 680+ FICO). Offers loans from $5,000 to $100,000 with competitive rates and no fees. They also offer unemployment protection. APRs can start around 8-9%.

- Upgrade Personal Loans: More accessible for borrowers with fair to good credit (580+ FICO). Offers loans from $1,000 to $50,000. APRs are higher, starting around 8-9% and going up to 35.99%, but they can be an option when other lenders won't approve you. They often have an origination fee (1.85% - 9.99%).

Typical Cost: Interest rates vary widely based on your credit score, loan amount, and term. Origination fees might also apply, especially for lower credit scores.

Common Credit Score Myths Debunked Separating Fact from Fiction

There's a lot of misinformation out there about credit scores. Let's clear up some common myths:

Myth 1 Checking Your Own Credit Score Harms It

Fact: This is false! Checking your own credit score results in a 'soft inquiry,' which has no impact on your score. Lenders' inquiries are 'hard inquiries' and can temporarily lower your score. So, feel free to check your score as often as you like.

Myth 2 Closing Old Credit Cards Boosts Your Score

Fact: Usually the opposite is true. Closing an old credit card reduces your total available credit, which can increase your credit utilization ratio. It also shortens your average credit history length, both of which can negatively impact your score. Keep old accounts open, especially if they have no annual fee.

Myth 3 Carrying a Balance Helps Your Score

Fact: Absolutely not. Carrying a balance on your credit card, especially if it's high, increases your credit utilization and costs you money in interest. The best practice for your score and your wallet is to pay your credit card balance in full every month.

Myth 4 All Debts Impact Your Score Equally

Fact: Not all debts are created equal. While all debts are considered, the type of debt and how you manage it matters. For instance, a mortgage is an installment loan and is viewed differently than revolving credit card debt. Also, how you pay (or don't pay) each debt has a different impact. A late payment on a credit card might hurt less than a foreclosure on a mortgage.

Myth 5 You Only Have One Credit Score

Fact: You actually have many credit scores! You have a FICO score and a VantageScore, and within each of those, there are different versions (e.g., FICO Score 8, FICO Score 9, FICO Auto Score, FICO Bankcard Score). Each credit bureau (Experian, Equifax, TransUnion) also generates its own version of these scores. Lenders use different versions depending on the type of loan. So, the score you see might not be the exact one a lender uses, but they are usually very close and move in the same direction.

The Future of Credit Scoring Emerging Trends and What to Expect

Credit scoring models are always evolving. Here's a peek at what might be coming:

Alternative Data Inclusion Broader Financial Picture

Some newer scoring models are starting to incorporate 'alternative data' like rent payments, utility payments, and even bank account transaction data (with your permission, of course). This can be a game-changer for people with thin credit files or those who have historically been underserved by traditional credit models. It provides a broader picture of your financial responsibility beyond just traditional loans and credit cards.

AI and Machine Learning More Accurate Assessments

The use of artificial intelligence and machine learning is becoming more prevalent in credit scoring. These technologies can analyze vast amounts of data to identify patterns and predict creditworthiness with greater accuracy. This could lead to more personalized credit offers and potentially fairer assessments for a wider range of consumers.

Financial Wellness Focus Beyond Just Debt

There's a growing emphasis on overall financial wellness, not just your ability to manage debt. Future credit assessments might look more holistically at your savings habits, emergency fund status, and general financial stability, rather than just your borrowing history. This shift could encourage more responsible financial behavior across the board.

Wrapping It Up Your Credit Journey

So, there you have it! A deep dive into credit score ranges, what they mean, and how they impact your financial life. Remember, your credit score is a journey, not a destination. It's something you build and maintain over time with consistent, responsible financial habits. Whether you're aiming for that 'excellent' tier or working your way up from 'poor,' every positive step you take makes a difference. Keep monitoring your scores, dispute any errors, and make smart financial choices. Your future self will thank you for it!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)